Economic Forecast: Highest growth in 27 years curbed by labour shortage

There are indications that the Danish economy will reach its highest growth rate since 1994. The reopening has gone incredibly well, which has caused a significant increase in employment and has led to an extensive shortage of labour. A labour shortage that is bound to reduce the growth rate as many companies find themselves either rejecting orders or being forced to supply their customers with imported products.

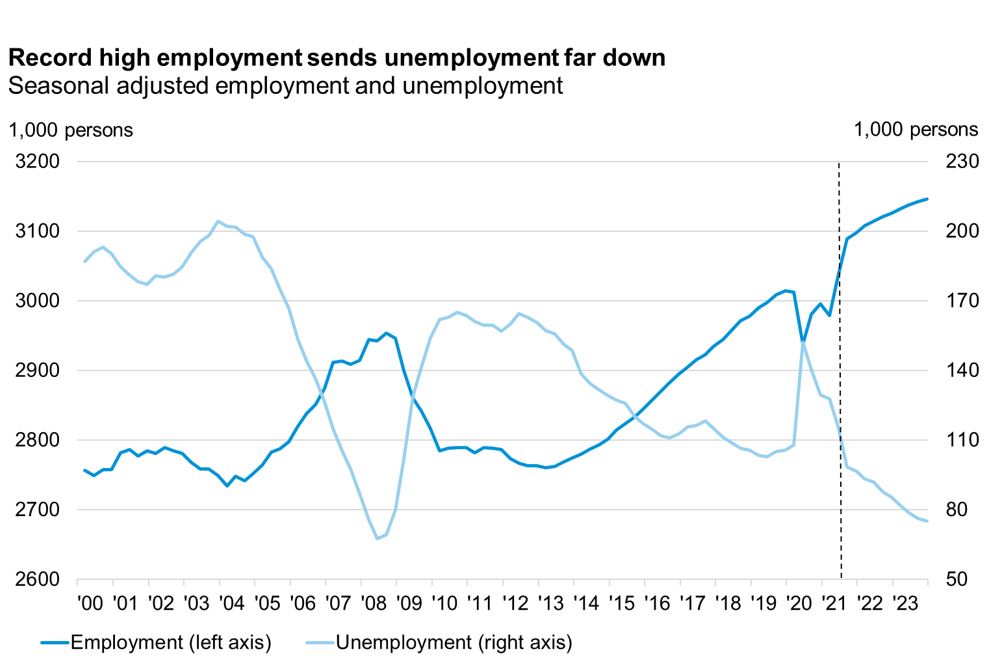

Employment has increased by 91,000 individuals from January to July 2021. This is, by far, the largest increase ever measured during a six-month period. The rapid growth in employment has drained the labour market, resulting in a drop in unemployment, in August, to its lowest level in 12 years.

Source: Statistics Denmark and DI

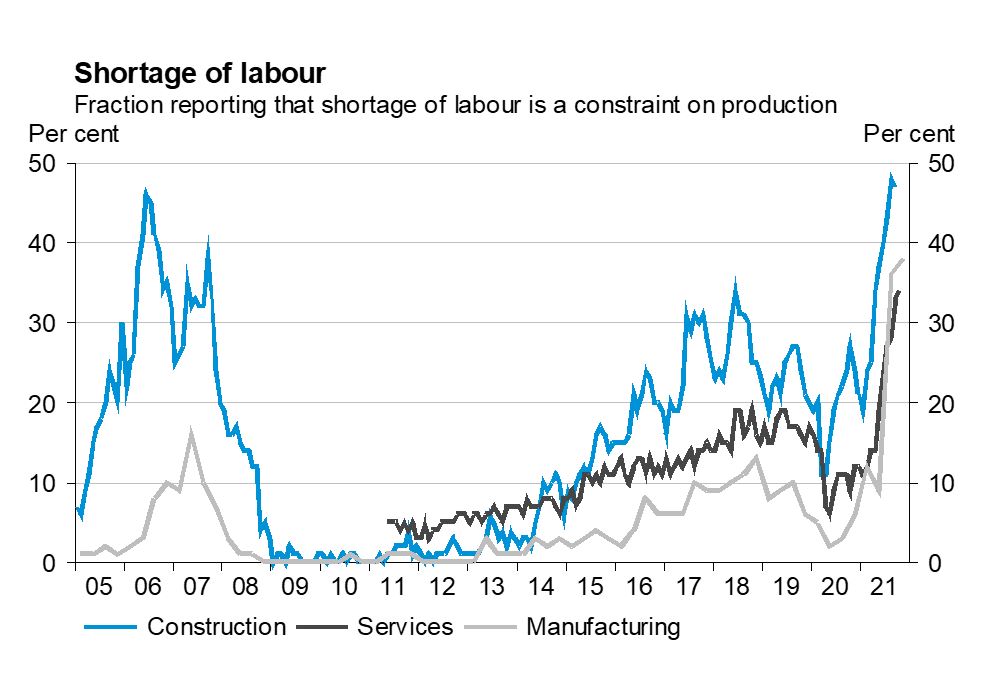

In both the manufacturing industry, construction and service sectors, companies are now reporting a shortage of labour higher than ever before.

Source: Statistics Denmark, latest observation Jan. 2020

Employment is expected to continue its increase in the coming years, but growth could have been even higher had companies not been hit by a shortage of employees. Even today, the Danish companies could have had 32,000 more employees had they not experienced challenges recruiting.

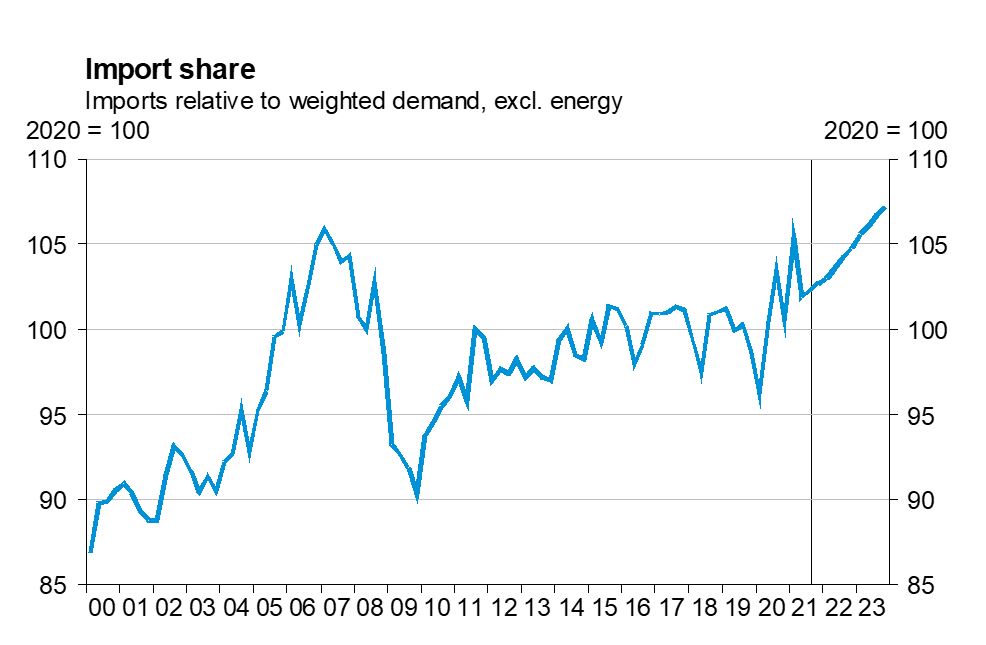

The last time we experienced a very extensive labour shortage was in 2006 and 2007, when unemployment plunged just as sharply as it is the case today. The experience from those years showed that a lack in production capacity led to deterioration in competitiveness and a substantial increase in imports.

From 2003 to 2007 imports of goods (energy excluded) increased by 15 percentage points more than demand. This additional increase was due to a combination of weak competitiveness and constraints in production as a result of the labour shortage.

Source: Statistics Denmark and the Confederation of Danish Industry

Together with the increase in imports, we experienced that industrial exports decreased by nine per cent relative to the foreign demand for industrial exports from 2003 to 2007. This too, may be attributed to a combination of weak competitiveness and limited production capacity.

Going forward, we expect to see some similar trends in the current situation. However, unlike the situation in 2006 and 2007, Danish competitiveness has not yet weakened. Also, the extent of relocation of Danish production is estimated to be lower than in the years leading up to the financial crisis.

With a better starting point, we expect the situation to be somewhat better than what we saw in 2006 and 2007. We therefore anticipate an increase in imports of goods (energy excluded) in relation to the demand in Denmark of 3.2 percent-age points through to 2023. Growth in industrial exports is ex-pected to be 5.4 percentage points lower than the increase in demand on the export markets.

The additional import of 3.2 percentage points corresponds to DKK 22bn. The reduction in exports of 5.4 percentage points equals DKK 26.7bn. Thus, Danish turnover is expected to be reduced by almost DKK 48.7bn, reducing incomes by almost DKK 25bn during the forecast period. Thus, growth and pros-perity would have been higher in the coming years, had it not been for the shortages of labour (and materials).

Highest level of growth since 1994

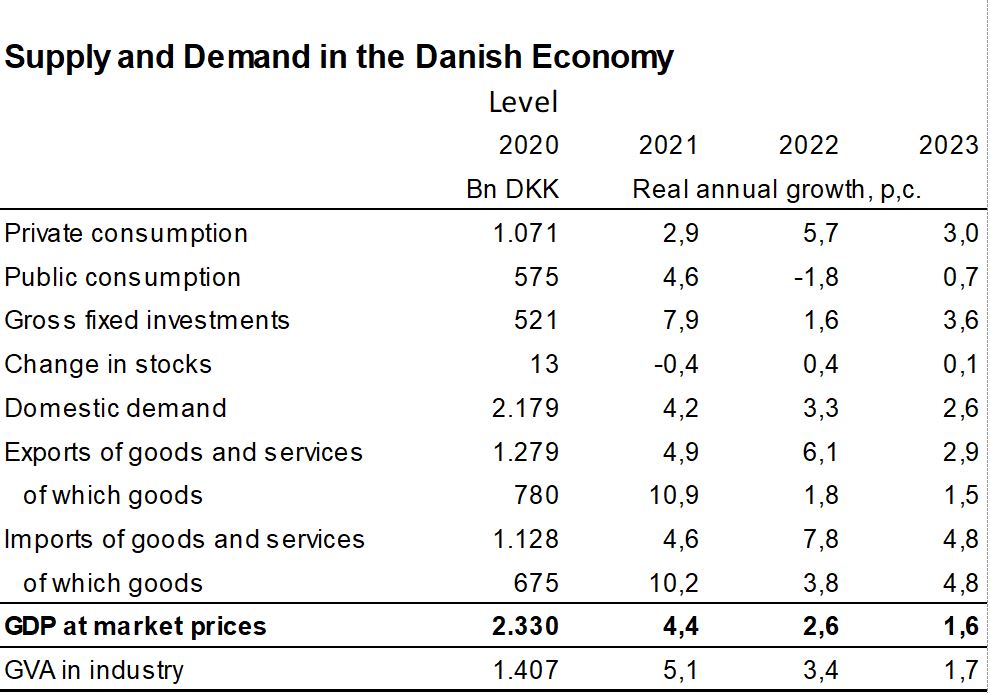

This year, the Danish economy is headed for its highest growth rate in 27 years having exceeded four per cent for the first time since 1994. The growth is broadly based on the increase in exports, investments, and private and public consumption.

The strong recovery will continue into 2022, with continued growth in both private consumption and exports, in particular. The expiration of part of the public measures against corona will result in a decrease in public consumption in 2022.

Note: Changes in stocks as a percentage of GDP in the previous year

Source: Statistics Denmark and the Confederation of Danish Industry

The availability of labour market resources will be dwindling during the forecast period putting growth under pressure. In 2022, the GDP growth rate will drop to 2.6 per cent and in 2023, the growth rate will drop below two per cent again.

Strong demand from abroad

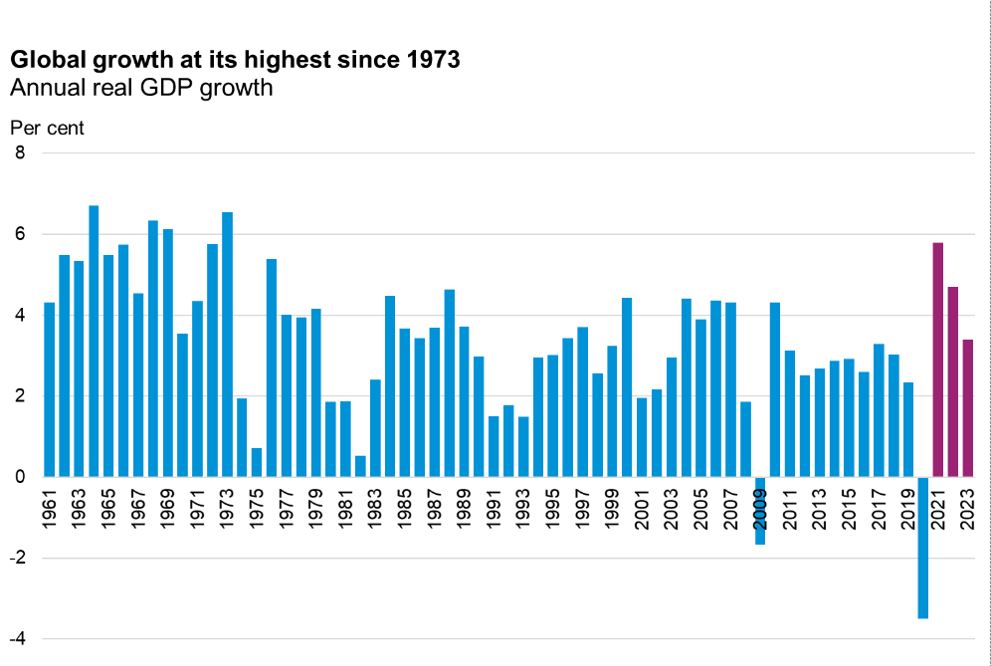

The world economy has been through a major turnaround. In 2020 the Corona crisis led to the biggest downturn since World War II, which in 2021 has been turned into the largest increase since 1973. Growth will also be high in both 2022 and 2023, however, declining towards somewhat more normal growth rates. It is a broad-based recovery with progress in all parts of the world.

An ever-increasing proportion of the world’s population has been vaccinated against corona, and the number of restrictions imposed in order to deal with the infection, is at its lowest level since last spring. Denmark is, in general, far ahead of many other countries in terms of roll-out of vaccines and removal of restrictions. Corona, however, still haunts and, among other things, causes disturbances in world trade with ports having been shut down (due to corona). The situation, however, has become so much under control, that it will not jeopardize the global recovery.

Source: World Bank and Oxford Economics

High levels of growth abroad provide fertile ground for increasing demand for Danish goods and services.

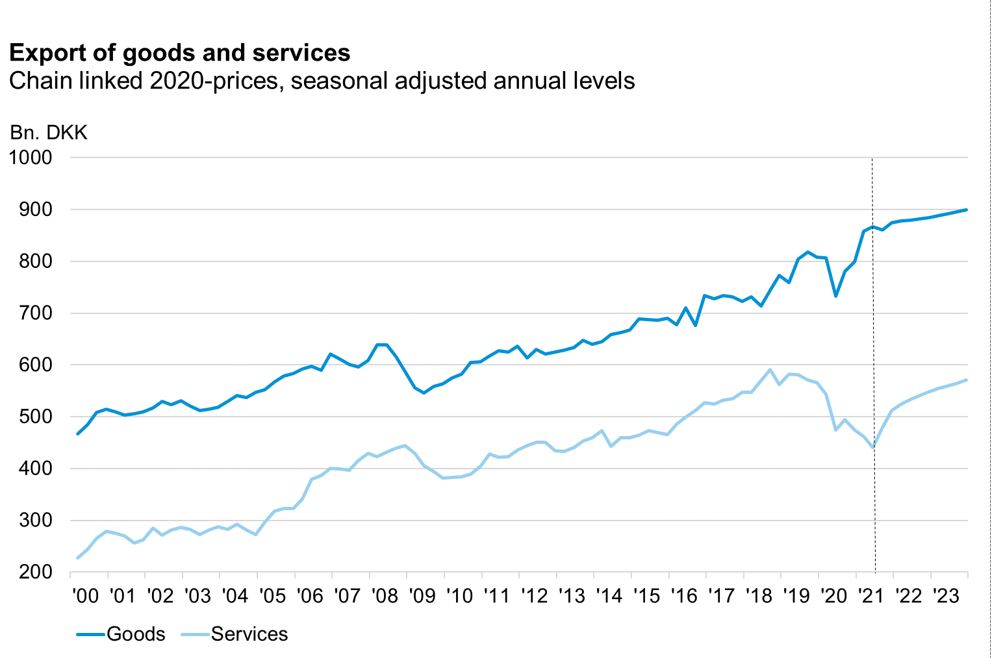

Already, exports of goods have done incredibly well the last year. Exports of goods have increased four quarters in a row and are currently 18 per cent higher than a year ago. Exports of goods will also increase in the coming years, but at a much slower pace due to shortage of labour and materials.

In recent years, industrial exports have grown faster than demand abroad, which means that we have gained market shares. A trend that has also been helped along by the particularly stable Danish exports with a relatively high content of, e.g., life-science, food and “green solutions”. It is expected that, going forward, we will lose market shares again, as the companies’ production restrictions mean that we will be unable to meet the entire increase in demand from abroad in the coming years. In the coming period, part of the increased demand from abroad will also be targeted at services with a lower Danish product content.

Source: Statistics Denmark and DI

Service exports have not yet gained traction and dropped in the second quarter to the lowest level since the beginning of 2013. Over the past year, service exports have dropped by seven per cent and is (currently) as much as 25 per cent lower than two years ago.

Service exports – not least aviation and tourism – have quite good prospects for growth in the coming years, as the normalization of consumption patterns and the easing of travel restrictions mean that more activities across national borders will resume.

On that basis, total exports will grow by close to five per cent in 2021, driven by substantial growth in exports of goods. In the coming years, growth in exports of goods will decline, while service exports are expected to provide a significant contribution to the overall growth in exports.

Private consumption has bounced back

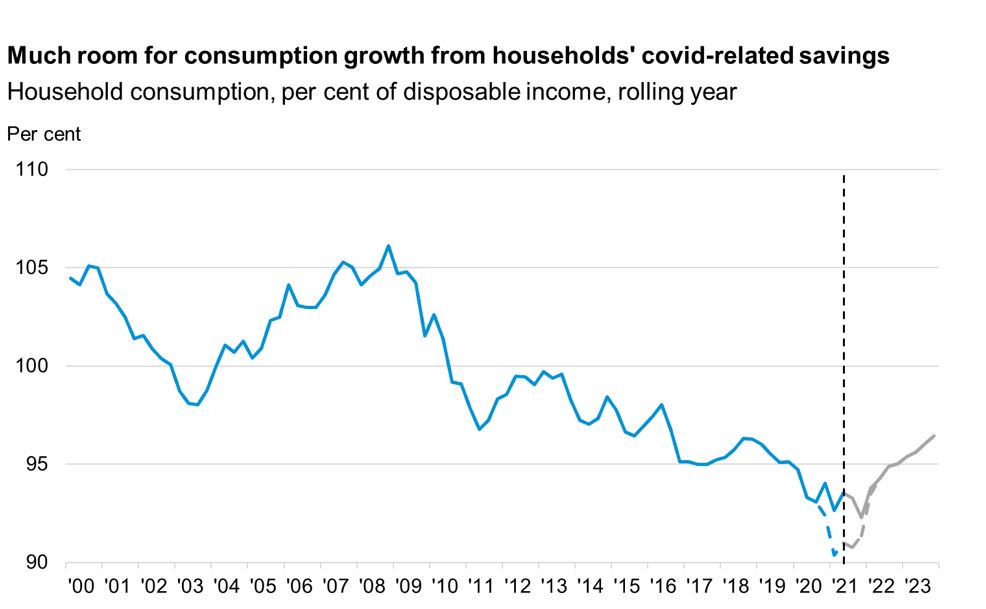

As expected, the gradual easing of restrictions and the lower level of infection during the spring has led to a strong increase in private consumption. Private consumption increased by 5.9 per cent in the second quarter and has returned to pre-crisis levels.

Despite second quarter’s strong growth, there is still plenty of room left for growth in the recovery of private consumption. Wage compensation, payment of the so-called “frozen” holiday pay and the increase in employment have boosted household incomes.

Note: The dashed line indicates the level of consumption when adjusting for extraordinary taxation in connection with the payment of frozen holiday pay in 2020Q4 and 2021Q1.

Source: Statistics Denmark and the Confederation of Danish Industry

Household’s disposable income is characterized by the extraordinary tax payments stemming from the payment of the “frozen”

holiday pay. When the extraordinary tax payments are disregarded, the consumption quota dropped to 90.9 per cent in the second quarter in comparison to 95.1 per cent prior to the crisis.

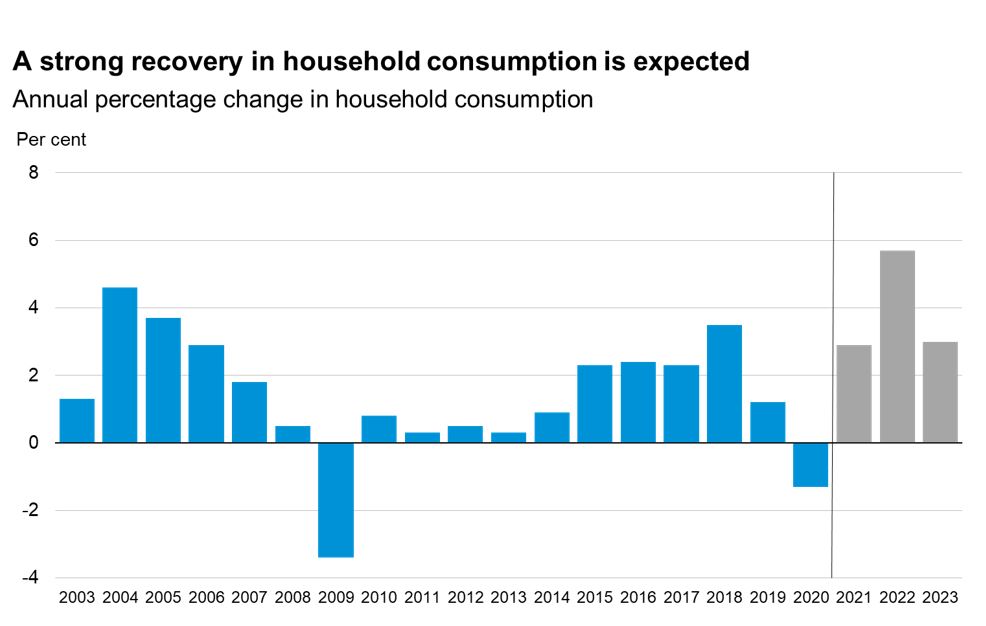

It is not only large savings accumulated during the shutdowns that may help boost private consumption. Increasing stock market prices and house prices have helped increase Danes’ wealth significantly. Thus, everything points to a strong recovery in private consumption, and DI estimates that private consumption will grow by 2.9 per cent in 2021, 5.7 per cent in 2022 and by 3.0 per cent in 2023.

Note: Real growth in 2021 and beyond are estimates on the basis of the forecast.

Source: Statistics Denmark and the Confederation of Danish Industry

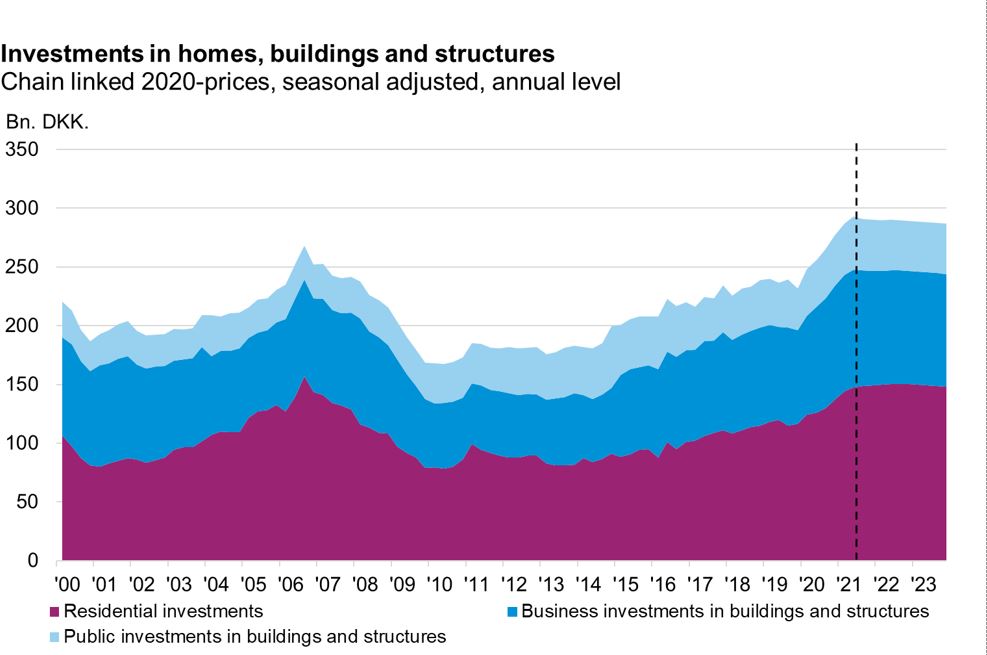

Capacity issues slow down construction activities and increase investments in equipment

The housing market has roared ahead during the corona crisis, since prices on houses and apartments have risen sharply. However, there are signs that the housing market is declining. Over the past few months, we have seen a stagnation in both prices and in the number of home sales, and the slightly higher mortgage rates are also expected to dampen the demand for housing.

Together with rising incomes, the high increase in house prices have contributed to increasing housing investments. This applies in particular to 2021, as investments in housing are expected to grow by as much as 14 per cent. This should also be seen in the light of the temporarily extended “Boligjobordning”, which is expected to have sped up the initialization of many projects. In addition, renovations in the public housing sector as a result of the so-called “Grøn Boligaftale 2020” are expected. Thus, in the coming years, a more subdued development in investments in housing is expected resulting in an increase of 1.7 per cent in 2022, followed by a decline of 0.7 per cent in 2023.

Source: Statistics Denmark and DI

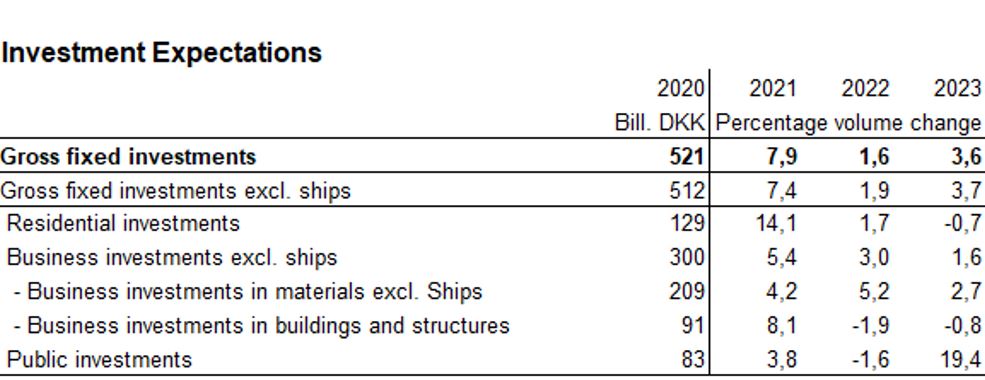

Businesses’ investments in housing, buildings and plants are expected to increase by 8.1 per cent in 2021 and then to drop by 1.9 per cent in 2022 and by 0.8 per cent in 2023.

The slowdown in investments in housing, buildings and plants must be seen in the light of the fact that these activities have reached a historically high level. Off hand, there seems to be demand for even more, but the building industry is facing major capacity challenges due to a historically large shortage of both employees and materials. Thus, there does not seem to be any room to increase activities, but on the other hand, the backlog of orders is so large, that a major decline in activities is not to be expected either.

Source: Statistics Denmark and the Confederation of Danish Industry

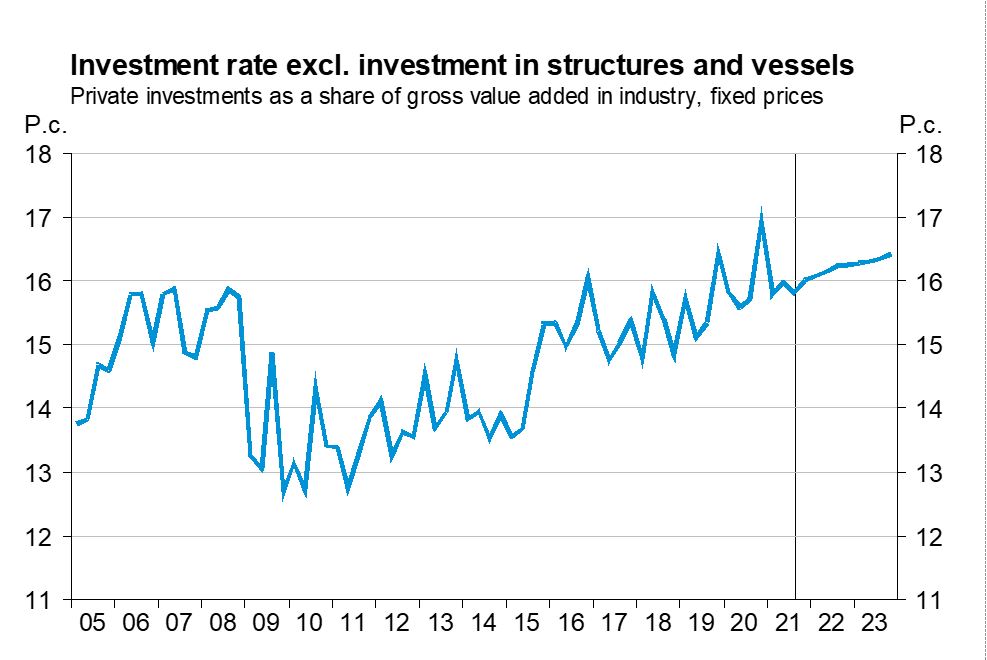

Companies’ investments in equipment, including machines and means of transportation, dropped sharply during both the first and the second shutdown, but have had a quick rebound on both occasions. An increase in investments in equipment (vessels excluded) of 4.2 per cent is expected in 2021. With the pro-spect of increased activity, both domestically and in our export markets as well as increasing capacity issues, investments in equipment are expected to increase by 5.2 per cent in 2022 and by 2.7 per cent in 2023. However, shortage of labour is likely to dampen companies’ necessary investments in for example both the green transition and digitalisation. As a consequence, the investment ratio will increase slightly in the coming years. However, it will remain roughly on the average trend since 2005.

Source: Statistics Denmark and the Confederation of Danish Industry

Companies’ total investments (vessels and animals for breeding excluded) is expected to increase by 5.4 per cent in 2021 and then to increase by a further 3.0 per cent in 2022 and by 1.6 per cent in 2023.

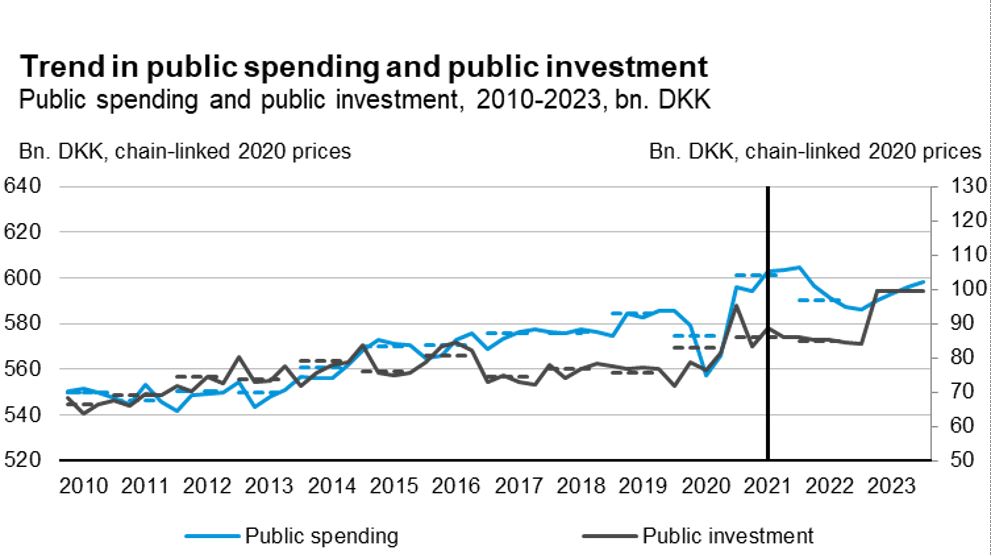

High level of public consumption

The level of public consumption underwent a significant increase in the fourth quarter of 2020 and has maintained a high level throughout the first half of 2021. The high level of growth in public consumption in 2021 can to a large extent be attributed to the corona crisis. Low activity in the first half of 2020 has been replaced by extensive test and vaccination efforts, resulting in a high level of public expenditure in 2021 – both in con-nection with the hiring of staff (especially in the first half of the year) and in connection with the purchase of vaccines, etc, lead-ing to a boost in growth in public consumption in 2021.

Note: The vertical dashed lines indicate annual averages. The level of public investment is shown on the secondary axis.

Source: Statistics Denmark and the Confederation of Danish Industry

In line with the estimate of the Ministry of Finance, it is our as-sessment that public consumption in 2021 will grow by 4.6 per cent. This is an extremely high level of growth, not seen since the late 1970s. As for 2022, a decrease of 1.8 per cent is esti-mated due to the lifting of the temporary corona restrictions. In 2023 a growth of 0.7 per cent is estimated following the devel-opment in the fiscal space.

Moreover, and still in line with the Ministry of Finance, we es-timate a growth in public investments of respectively 3.8, -1.6 and 17.4 per cent in the forecast years. The extremely high level of growth in 2023 should be seen in the light of the fact that a large delivery of fighter aircrafts is expected. Thus, the high level of growth is driven by public investments in equipment.

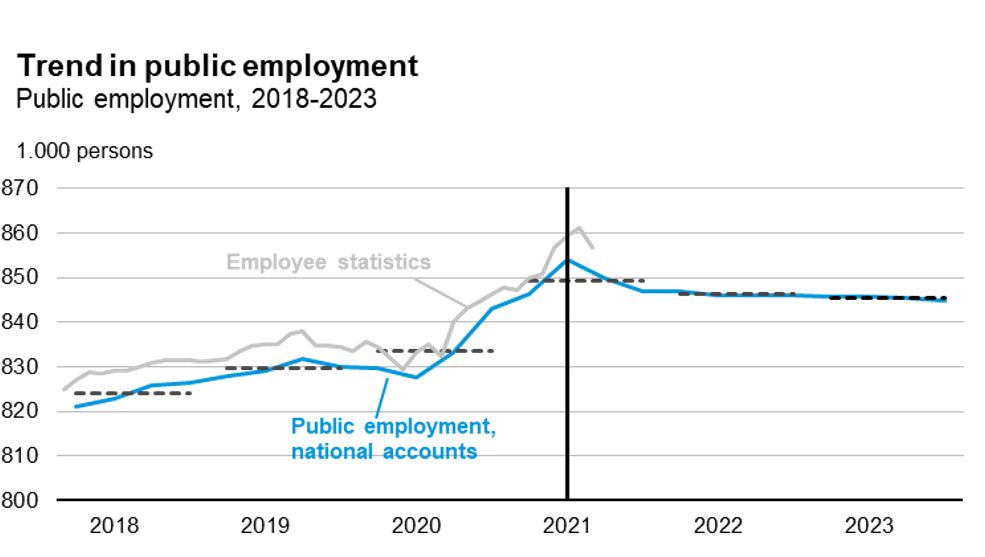

As mentioned, the influence of the corona crisis is clear in the development of public employment. In the national accounts, public employment has increased by 24,200 individuals to a record level since the fourth quarter of 2019. Figures from July on public sector employment indicate that public employment has started to decline, but it is still too early to conclude wheth-er this marks a turn in development or whether it is a temporary decline.

In line with the forecast of the Ministry of Finance, we expect a decline in public employment of 7,200 (individuals) in the remainder of 2021 as well as a limited decline throughout 2022 and 2023. As a result, in the fourth quarter of 2023 public employment is approximately 9,000 individuals lower than in the second quarter of 2021.

Thus, public employment is expected to remain at a high level in both 2022 and 2023 regardless of the decline due to the cessation of temporary employment linked to the corona crisis.

Note: The vertical dashed lines indicate annual averages.

Source: Statistics Denmark and the Confederation of Danish Industry

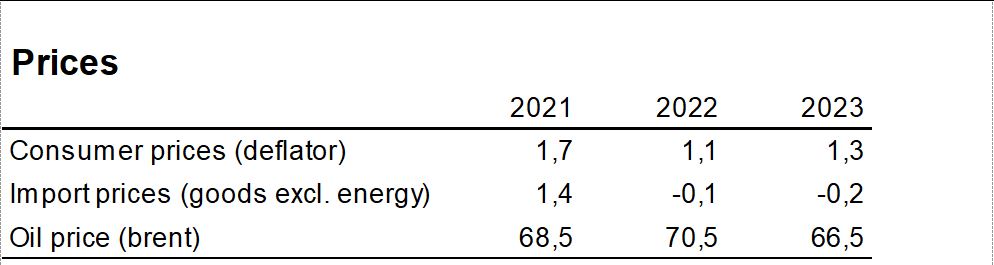

Sharp increase of various prices

The prices on a wide range of raw materials as well as freight rates have risen sharply, especially in the first half of 2021. Recently we have seen sharp increases in the prices on natural gas.

As a consequence, the increase in prices has led to the highest rate of increase in Danish consumer prices since 2012. However, the inflation rate in Denmark remains below two per cent. There are indications that the prices of a wide range of commodities will fall slightly again.

Source: Statistics Denmark and the Confederation of Danish Industry

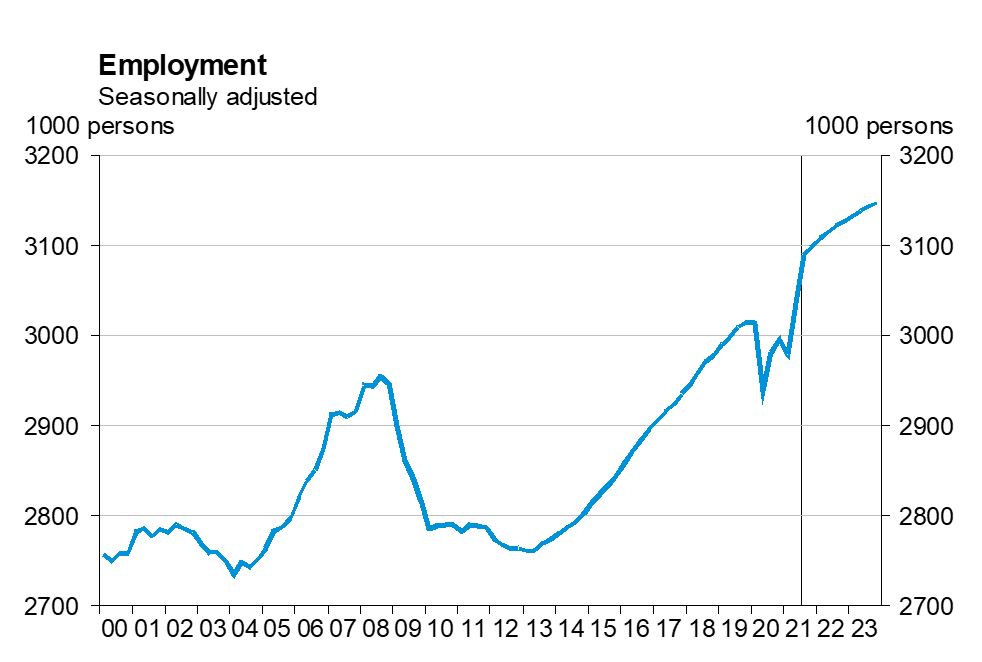

Many records in the labour market

The labour market got through the first year of corona rather well in comparison to the economy in general. In addition, there has even been a large increase in employment during the spring and the summer causing the number of employees in July to arrive at 51,000 individuals above the previous record level from before the corona crisis. In total, employment has increased by as much as 130,000 individuals from the bottom of the crisis in May 2020 to July 2021. Thus, indicating a labour market in strong growth.

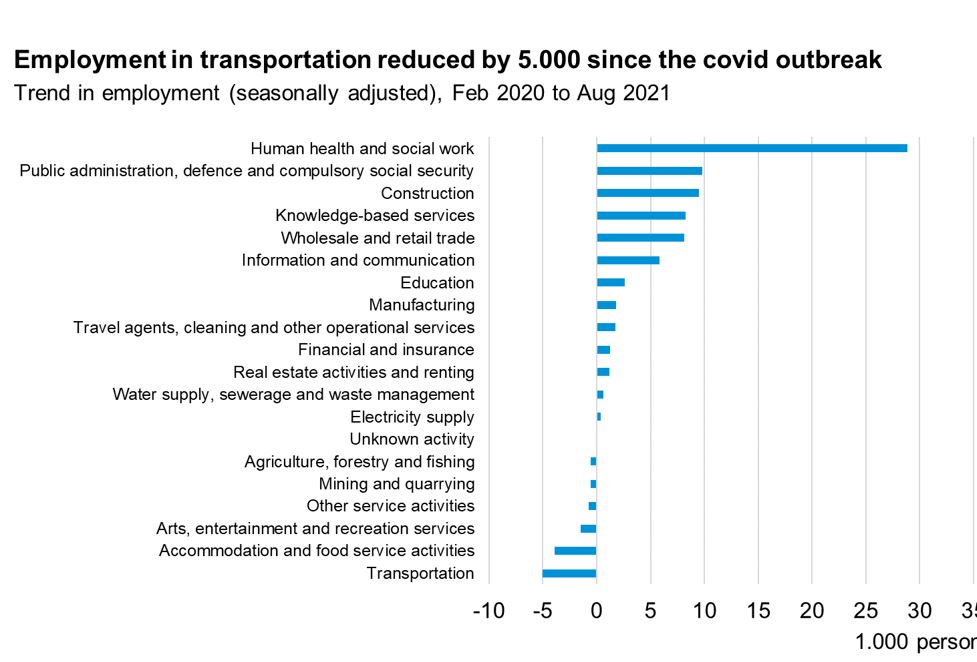

The development in employment during the corona crisis has varied widely from sector to sector, but almost all sectors have benefited from the recent progress. Most sectors have now more than made up for lost jobs during the crisis. The sectors that were hit the hardest during the crisis are also the sectors who have undoubtedly had the greatest growth in employment during spring and early summer. This applies to hotels and restaurants as well as culture and leisure, which now trail previous employment levels by only 4,000 and 2,000 individuals.

Source: Statistics Denmark

All in all, the development in employment from February 2020 to July 2021 shows an increase in employment of 29,000 individuals in the private sector and an increase of 22,000 individuals in the public sector. Thus, as mentioned earlier, the public sector’s share of employment has increased.

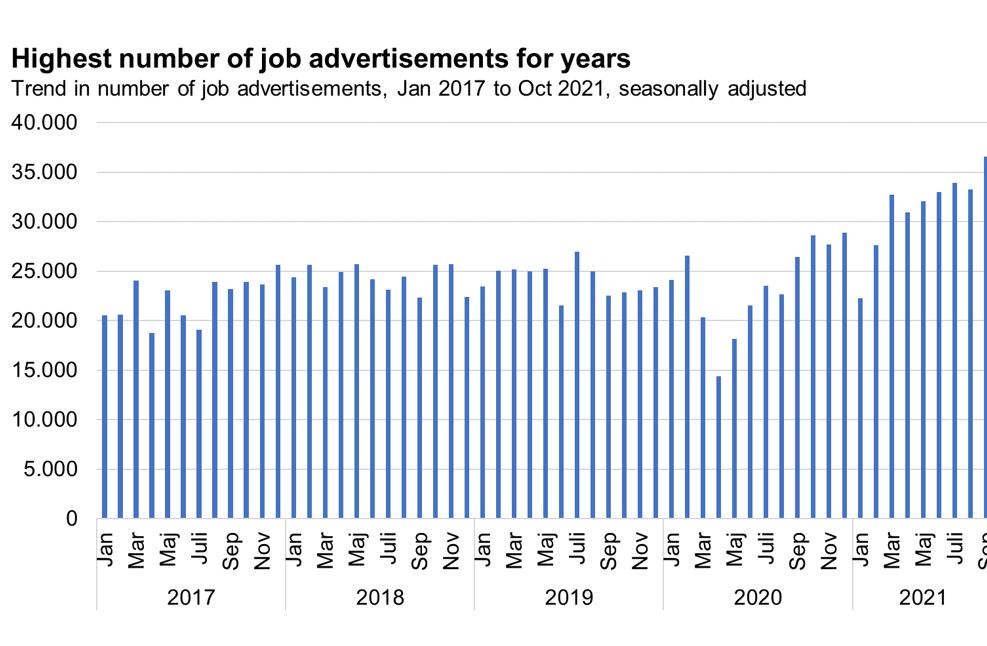

The development in the labour market through spring and summer shows a labour market in which the recovery is well underway. A fact that is seen not only in employment, but also in the large number of new job adverts, which is at its highest level in years. During the past six months, as many as 200,000 job adverts have been posted. In September this number has reached a monthly level that is not seen higher in more than 14 years.

Source: jobindex.dk (seasonal adjustment by the Confederation of Danish Industry)

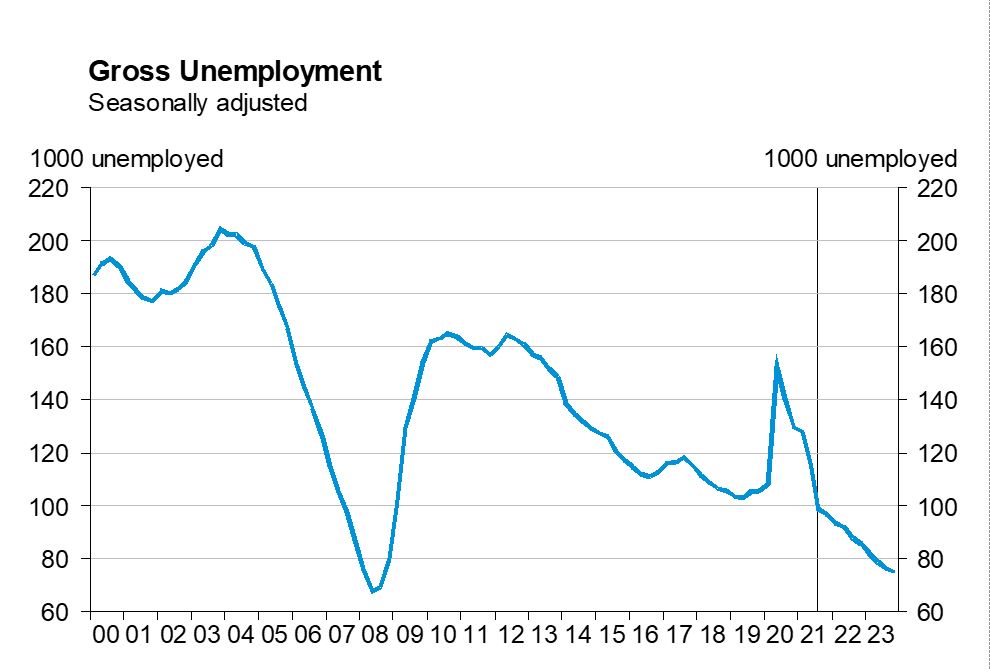

In August unemployment dropped to the lowest level in 12 years. A further decline in unemployment is shown for September in the Ministry of Employment’s latest daily figures for the number of registered unemployed, which runs until mid-September.

Shortage of labour is currently the biggest challenge for companies in relation to growth. Six out of ten companies lack qualified employees to such an extent that it challenges their possibilities for growth. The lack of qualified employees is by far the biggest growth challenge overall and across sectors and regions. A recent survey among DI member companies from September shows that companies would hire 32,000 more employees if the candidates were available, and that the shortage of labour has worsened significantly during the past three months, seeing that the number is almost twice as high as the number for June.

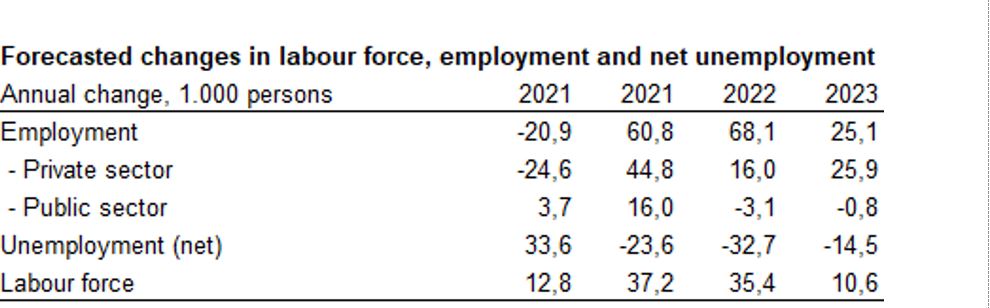

The current positive development in employment is expected to continue uninterrupted through the rest of 2021. According to DI’s forecast, employment in 2021 will be overall 68,500 higher than in 2020. A further increase in employment of 67,000 individuals is expected during 2022, while the increase in 2023 is expected to reach approximately 22,500 individuals due to lower, yet still positive, growth rates through 2022 and 2023.

Source: Statistics Denmark and the Confederation of Danish Industry

In February 2020, prior to the corona crisis – unemployment was at 3.6 per cent. Towards May 2020 it rose sharply to 5.5 per cent. In August 2021, unemployment was down again to 3.6 per cent. In the coming months we expect unemployment to continue its decline. DI expects that for the whole of 2021, unemployment will be 22,700 individuals below the level in 2020. As for 2022 and 2023, unemployment is expected to decrease respectively by a further 20,100 individuals and by 11,700, meaning that in 2023 unemployment will be approaching the lowest level ever measured.

Source: Statistics Denmark and the Confederation of Danish Industry

In 2021, an increase in the workforce of 37,200 individuals is expected. As for 2022 the number is 35,400 and in 2023 a further 10,600 individuals is expected. Later retirement age and the influx of foreign employees have had a positive effect on the workforce, while on the other hand the introduction of early retirement (for some) will have a negative influence from 2022 and onwards. Companies are in great need of more qualified employees which means that the introduction of a new early retirement scheme comes at a most unfortunate time. Without early retirement, both workforce and employment would increase more in both 2022 and 2023.

Source: Statistics Denmark and the Confederation of Danish Industry

Approach

This economic forecast is based on published Danish and international statistics on national accounts, foreign trade, financial conditions, etc. We have applied the macroeconomic model MONA when carrying out this forecast. MONA has been developed by the Danish Central Bank. However, this forecast and its assessments, are solely the responsibility of the

Confederation of Danish industry.

The forecast has been finalized on Monday, 4 October 2021.