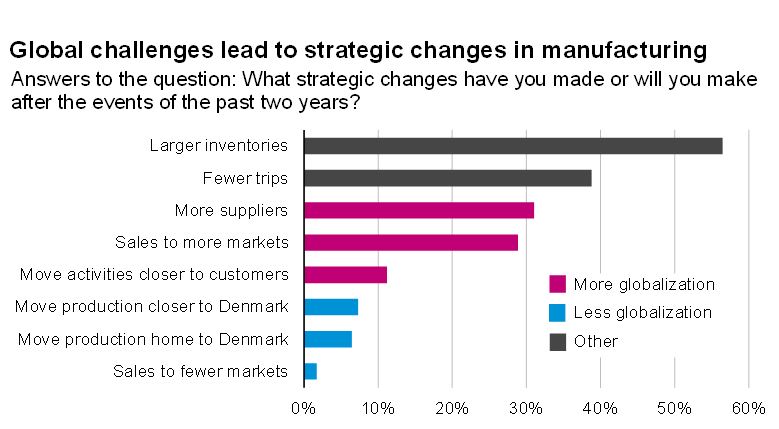

After two years of disruptions: Higher inventories and more suppliers

After two years with large and comprehensive disruptions in international trade, more than 8 out of 10 manufacturing companies make changes to their strategies. The solution is more globalization, not less. Many companies want to increase the number of suppliers and expand sales to more countries while few choose to reshore or sell to fewer countries.

More than 8 out of 10 Danish manufacturing companies have made or want to make strategic changes after two turbulent years with a pandemic, large supply disruptions and a war in Europe. This is according to a new survey among a large sample of DI’s manufacturing companies.

Note: The figure shows answers from exporting manufacturing companies in Denmark.

Source: DI Survey, 232 answers in February and March 2022.

Most companies with export activities have made or plan to make strategies for larger inventory levels and a third of the companies want more suppliers. However, only 7 per cent of the companies have decided it should be a strategic priority to move the production closer to or home to Denmark.

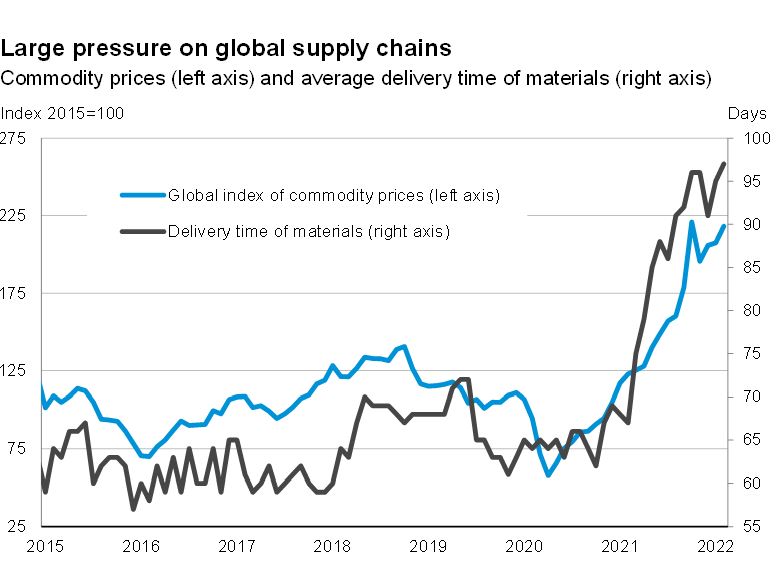

The strategic changes shall be seen in the light of the last two years’ large and comprehensive disruptions in international trade. The pressures on global supply chains have been extraordinarily large. First, the COVID-19 crisis in spring 2020 caused closures, production stops and travel restrictions. Then, supply bottlenecks followed due to a slow reopening of the global supply chains and a significant shift of global demand towards physical goods. And recently, the Russian invasion of Ukraine has put additional pressures on global supply chains.

The pressure on global supply chains has led to shortages of materials which is evident in the expected delivery times. In the United States, the average delivery time for materials was 65 days prior to the COVID-19 crisis. During the last year, delivery times have increased by 30 days such that companies must now expect that it takes around 100 days before their materials can be delivered.

Source: Macrobond

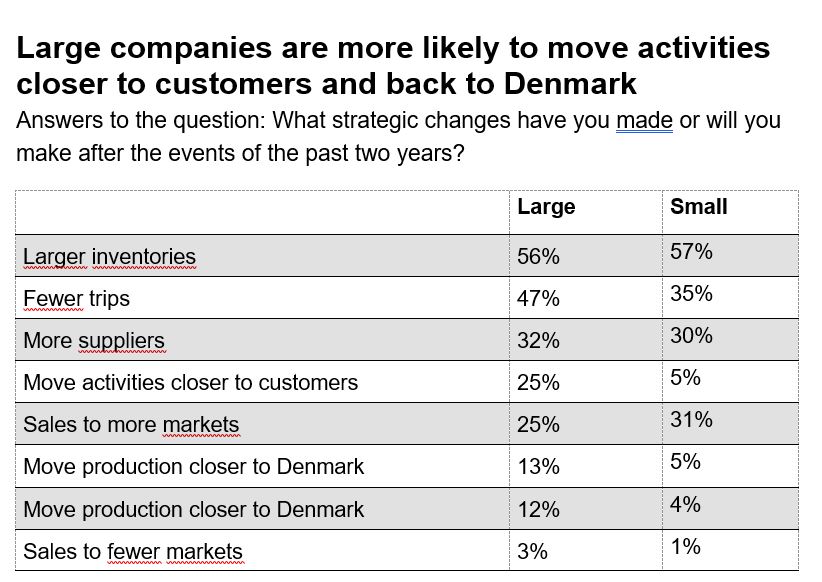

Both large and small companies make changes

Large companies will to a similar extent as small companies increase inventory levels and the number of supplies. Larger inventories and more suppliers mitigate the effects of future disruptions in international trade. Foreign studies document how companies with relatively high inventories had a smaller drop in production and sales than companies with relatively small inventories when the COVID-19 crisis hit.1

Large companies will, however, to a larger degree than small companies move their activities closer to their customers or back to Denmark. This can primarily be explained by the fact that large companies often have activities outside of Denmark which is a prerequisite for reshoring. Still, there are twice as many large companies that want to embrace global opportunities with more markets and suppliers than there are companies wanting to move activities to or closer to Denmark.

Note: Large companies are defined as companies with more than 100 employees. The table shows answers from exporting manufacturing companies.

Source: DI Survey, 232 answers in February and March 2022.

Note: The figure shows answers from both exporting and non-exporting companies.

Source: DI Survey, 522 answers in February and March 2022.

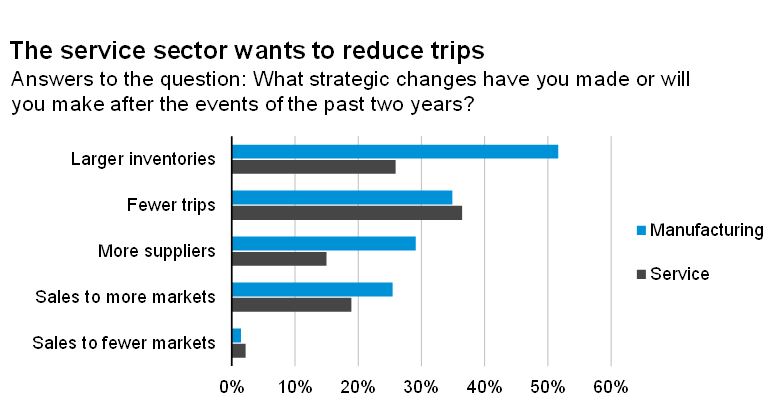

The strategic changes vary from sector to sector. In the service sector the events of the last two years have led to fewer travels. Travel restrictions and fewer physical meetings have highlighted the opportunities of more digital working. The adaptation of video conferencing, higher transportation costs and larger climate concerns are contributing factors when a third of all companies in the service sector want to reduce their trips going forward.

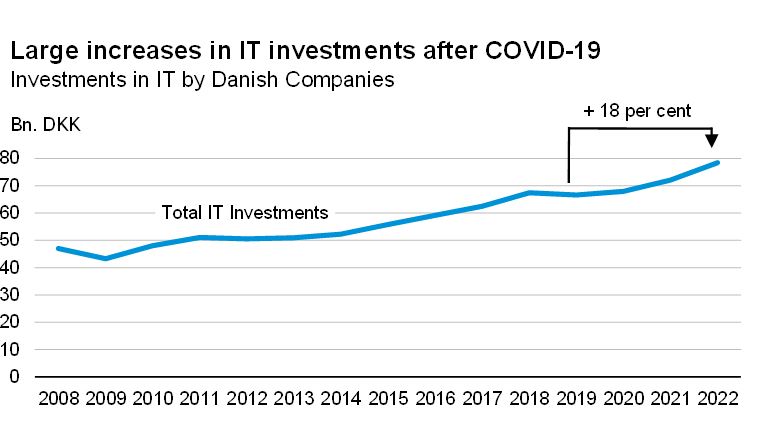

In general, the COVID-19 crisis has taught us how to work and shop online, increasing the need for digitalization in many companies. More companies have made digitalization a strategic priority. This shows in the companies’ yearly IT investments which have increased by 18 per cent since the start of the COVID-19 crisis. In addition, a study by DI shows that more than 7 out of 10 companies that emerge strengthened from the crisis have increased their use of digital solutions.2

Note: 2022 numbers are forecasted. See more in the DI study "Investeringer i digitalisering og IT fylder stadig mere i virksomhederne"

Source: DI and Statistics Denmark

The pace of globalization has slowed down

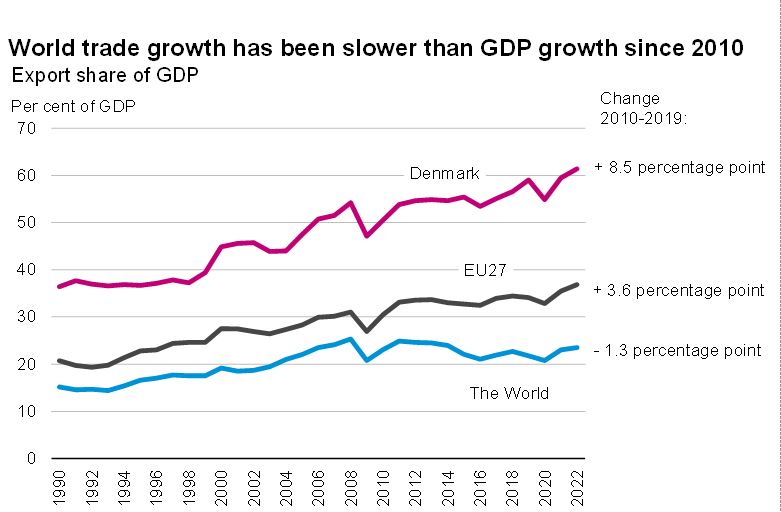

Since the financial crisis, globalization has slowed down. In the 1990’s, the marketization of economies in Asia and Eastern Europe led to large changes in global supply chains. An increasing share of the world’s total production moved eastwards and this increased the pace of world trade. The export share of global GDP grew from 15 per cent in 1990 to 24 per cent in 2007. However, since the financial crisis the pace of growth in world trade has not kept up with that of global GDP, and this year the export share is expected to amount to 23 per cent. In the case of Denmark the trade with the rest of the world has increased faster than GDP both before and after the financial crisis.

Note: An increase in the export share implies that exports grow faster than GDP. 2022 numbers are forecasted.

Source: DI, UNCTAD, Oxford Economics and Statistics Denmark.

There are no signs of an actual cancellation of globalization despite the last two years’ events. On the contrary, the answers from DI’s survey show that relatively few companies have moved or want to move production closer to or home to Denmark. Instead, the companies want to do business with more markets and expand the number of supplies such their supply chains are less vulnerable to regional closures. Almost every fifth company want to sell to more markets while very few want to sell to fewer markets. This suggests that we will see more globalization and not less.

However, there are EU tendencies that may lead to more regional supply chains in the next decade. EU’s new and more active industrial strategy aim towards more strategic independence from the rest of the world and higher competitiveness within important industries. There are certain areas where Europe wants to “be on its own”. With the new industrial strategy the EU wants to secure the European technological interests in a world affected by trade tensions, geopolitical conflicts, and challenged supply chains. More “regional globalization” may also be more widespread if companies are reluctant to have their supply chains in countries that may be affected by sanc-tions in possible future conflicts.

The overall gains from global supply chains are large

There are many gains from global supply chains. They increase overall productivity and wealth because companies become specialized and do what they are best at. Without this specialization it would be much more expensive and difficult to perform complicated production processes from the mining of commodities to manufacturing and delivery of services.

The overall gains from being part of global trade networks far outweigh the costs that have been incurred during the last two years’ challenges. Several new studies show how all countries are better off being part of global trade networks rather than not being part of them – even when the global supply chains are under pressure.3 Small and open countries such as Denmark and Ireland have the largest gains.

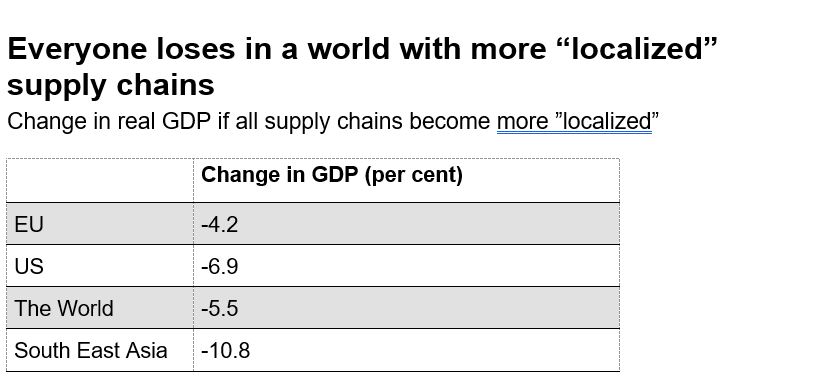

Less globalization in the form of less trade between countries have negative economic consequences, all else equal. A new study from OECD assesses that global GDP will be 5.5 per cent lower if all supply chains become more “localized”, i.e. that all countries in general increase domestic production at the expense of international trade.4

Source: OECD

Notes

- See the paper “Supply shocks in supply chains: Evidence from the early lockdown in China” from 2021 by Lafrogne-Joussier et al.

- See the DI study “En del virksomheder venter at komme styrket ud af krisen – andre er hårdt ramt” from March 2021.

- See the World Bank analysis “Measuring Exposure to Risk in Global Val-ue Chains” from 2021 by Borin et al or the article “Decoupling Global Value Chains” from 2021 by Eppinger et al.

- See the OECD analysis ”Global value chains: Efficiency and risks in the context of COVID-19” from February 2021.