Economic Forecast May 2022 - Danish economy is slowing down, but at a high level-

The Danish economy began 2022 from a very high starting point, however, restrictions on production, high rate of inflation and weakened demand mean that we will see a dip during the summer. DI estimates that at the end of the year, the GDP will be slightly lower than last year, while 2023 will offer a modest growth of 1.5 percent. Despite the decline, the level of activities as well as labour shortages will remain at a high level.

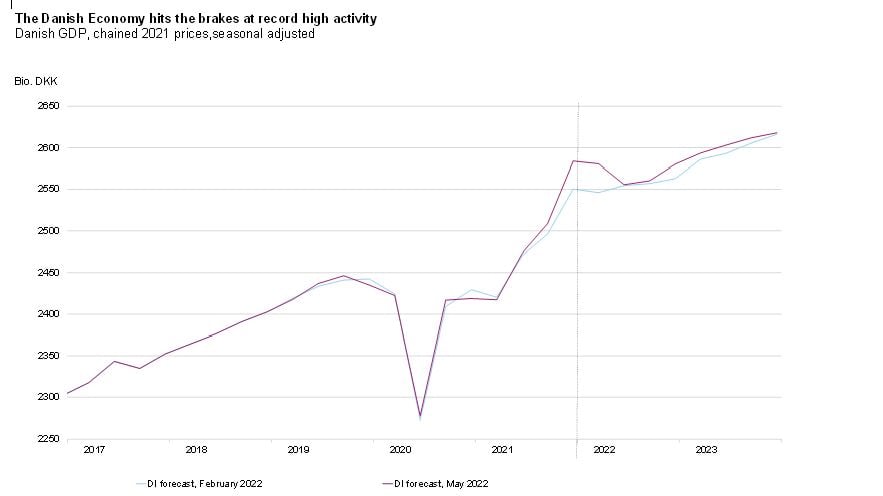

The Danish economy began 2022 at a high level of activity. In the fourth quarter of 2021 the GDP increased by as much as 3 percent, which means that we got off to a very good start in 2022. However, the high level of activity rests on a very uncertain base. Across all industries, historically large constraints on production due to a shortage of both labour and materials are reported, while at the same time demand appears to have suffered a setback. Therefore, sometime during the summer, DI expect to see a drop in the level of activity, but activity will remain at a high level.

Source: Statistics Denmark and DI

The war in Ukraine dampens aggregate demand as consumers are having their purchasing power eroded due to the high level of inflation. This is the case both in Denmark and abroad. At the same time, the acts of war and the sanctions imposed are having major impacts on exports to Russia and Ukraine. In addition, the lack of materials has increased resulting in the cancellation of some construction activities due to very high prices on building materials and increasing interest rates.

More companies will experience a lack of demand as a production constraint. However, for the vast majority of companies, this will primarily mean that their currently very long delivery times will be shortened somewhat. However, for those who are now being affected by a lack of demand, this slowdown is obviously not welcome.

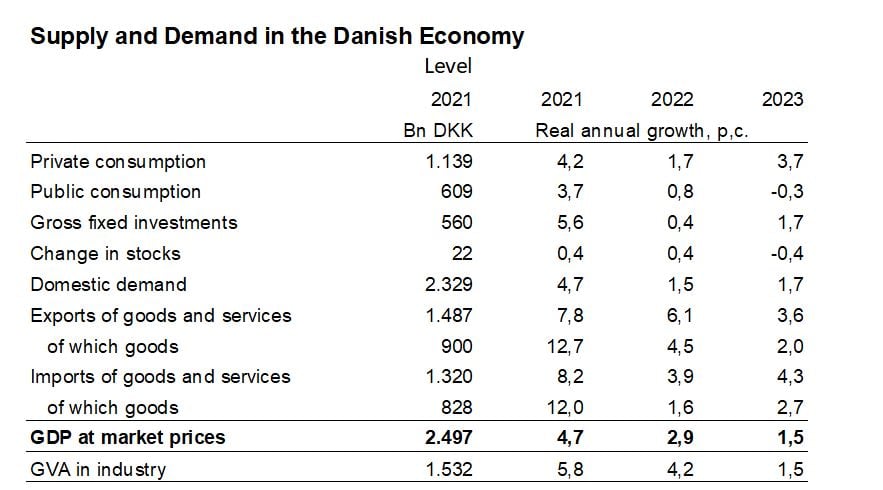

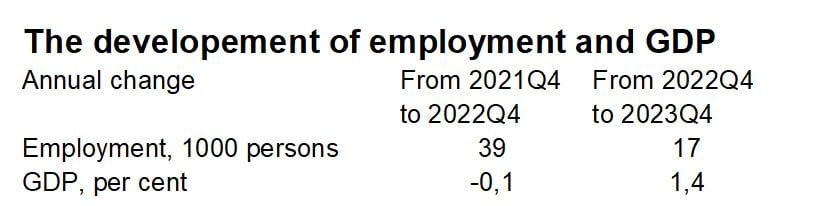

Overall, when measured on an annual basis, the Danish economy is estimated to grow by 2.9 percent in 2022. At first glance this appears to be quite a nice level of growth, but it covers for the fact that the growth is being helped by an incredibly strong starting point. Economic activity throughout 2022 will be lower than at the end of 2021. From the fourth quarter of 2021 to the fourth quarter of 2022, GDP is estimated to decrease by 0.1 percent. In 2023, a growth of 1.5 percent is expected – this being the case when measured both as an annual average and from the fourth quarter of 2021 to the fourth quarter of 2022.

Note: Changes in stocks as a percent of GDP in the previous year

Source: Statistics Denmark and the Confederation of Danish Industry

It looks as if employment has continued upwards in the first half of 2022, despite the fact that a decline in GDP is being estimated for the same period. Some companies are still experiencing growth and are therefore recruiting new employees. At the same time, companies that are experiencing a decline are reluctant to lay off employees that they may need again later. The number of job adds indicates that the increase in employment will continue in the future, but we expect the growth to be significantly more subdued than in the previous year.

Note: In the first quarter of 2022 employment rose by 26.000 persons

Source: the Confederation of Danish Industry

In the second half of 2022 and until next year, the prospects are for modest growth in the economy. A growth just large enough to ensure that unemployment does not increase. Therefore, an unchanged and still very significant pressure on the labour market throughout the forecast period is expected. However, it must be emphasized that this assessment is subject to considerable uncertainty.

High level of price increases, not least on energy, slows down growth

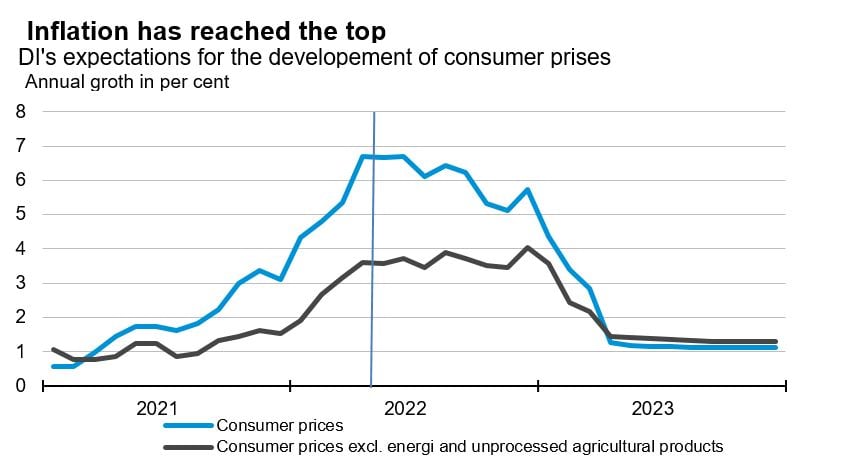

For many years, we have gotten used to a very stable level of prices. On average the consumer prices increased by just 0.8 percent per year in the period from 2013 to 2021. Inflation has undergone a sharp increase and is currently at its highest level in almost 40 years. In April, consumer prices rose by 6.7 percent. The inflation rate can mainly be attributed to the prices on energy. Also, prices on a number of unprocessed raw materials, including cereals and corn, have risen sharply. The rate of price increases was already high prior to the invasion of Ukraine but has undergone a further increase in connection with the war.

It is assumed that the prices of energy and unprocessed raw materials will remain more or less at the current level for as long as the conflict lasts. However, this means that the contribution to inflation will decrease as we reach periods where energy prices etcetera were already high a year earlier.

For prices other than on energy and raw materials we expect that there will continue to be a tendency for those higher prices on energy and raw materials to be included in the prices of finished goods. This tendency, however, will also gradually diminish. It is therefore expected that in the coming year we will see a very significant decline in the rate of inflation even with an unchanged high level of prices. However, there are generally price increases in certain areas, for example, rent.

In March a barrel of Brent oil cost just over USD 105 a barrel and the prices on oil futures suggest that the price will fall below USD 100 during the next six months. In April, Danish producer prices on raw material extraction and on energy fell. This could indicate that the pressure from the high prices on energy and on raw materials is finally easing. Should prices on energy and on commodities fall, it will have a direct negative contribution on inflation. However, even without a decline in these prices (as assumed in the forecast), the rate of price increases will decline sharply after December 2022, cf. the graph below.

Source: Statistics Denmark and the Confederation of Danish Industry

DI estimates that inflation (calculated at total consumer prices) will amount to 5.8 percent in 2022. Inflation is expected to decline to 1.7 percent in 2023.

Weakened exports

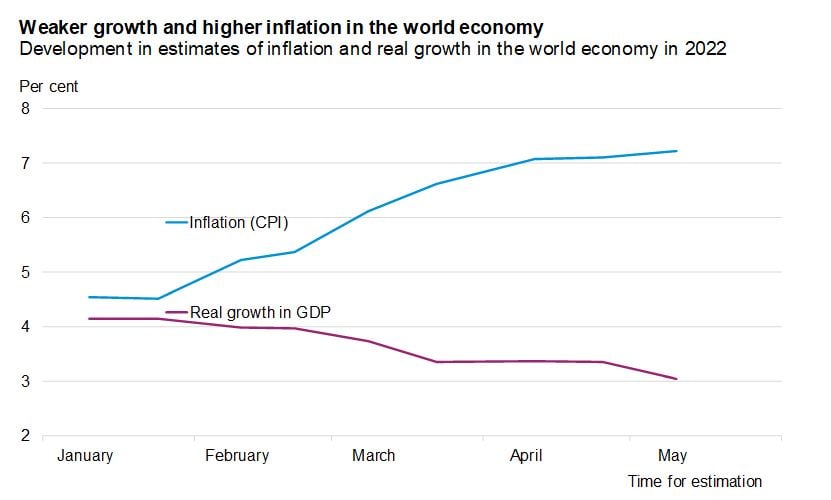

When it comes to exports, the prospects have weakened noticeably in recent months. During the first months of the year, Oxford Economics has downgraded its expectations for growth in the world economy in 2022. At the beginning of the year, growth of more than four percent in the current year was expected, but at the beginning of May growth expectations have been lowered to just three percent in 2022.

The biggest downgrades are undoubtedly related to the war in Ukraine. Massive decline in economic activity is expected in both Ukraine and Russia. In addition to the parties directly involved in the war, European countries have experienced the most substantial downgrades due to the war in Ukraine and to the restrictions imposed.

There is no longer being paid much attention to corona, but it still haunts and affects growth especially in China. The Chinese approach against the corona infection is very harsh. Ports and major cities have been closed down. This dampens growth, especially in the second quarter. For the year as a whole, a growth of four percent is expected, which is lower than expected at the beginning of the year. It is also a low level of growth by Chinese standards.

The US economy began the year with a slight downturn in the economy, but it is especially the high rate of inflation and the prospect of a sharp tightening of the monetary policy that have weakened growth prospects in the US. In April, US consumer prices had risen by 8.3 percent compared to the previous year. Inflation has risen more than expected, prompting the US Federal Reserve to forecast interest rate hikes of a total of 2.5 percentage points during 2022 and 2023. So far, the US Federal Reserve has raised interest rates by 0.75 percentage points. Their counterparts in the European Central Bank are still holding back, but it is expected that ECB will start raising interest rates at some point during summer.

It is the rapidly rising inflation that has put central banks under pressure to raise interest rates and curb the sharp increase in prices. During 2022, inflation has risen far more than expected. The expectations of global inflation have been raised from less than five percent at the beginning of the year to currently over seven percent.

Source: Oxford Economics

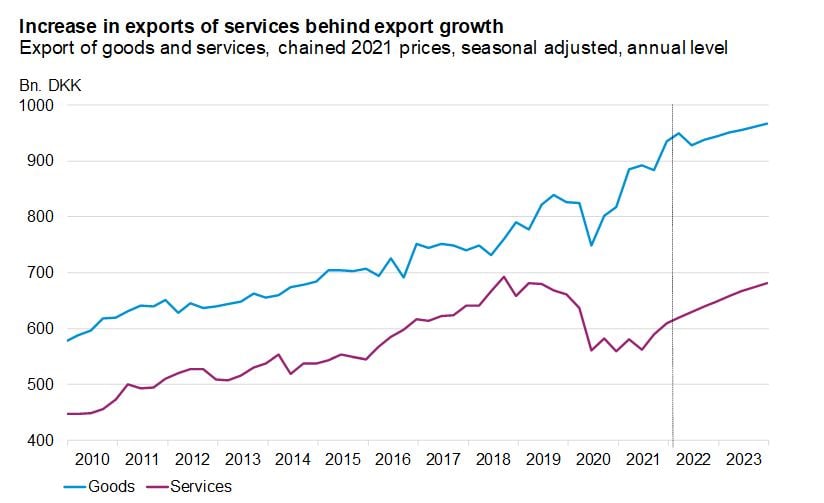

The war in Ukraine, the sanctions imposed, uncertainty, high level of inflation and the lack of materials weaken growth abroad and thus businesses’ export opportunities. Exports of goods have done quite well through the corona crisis but are expected to undergo a considerable slowdown in the time to come.

Exports of goods will face some obstacles in the second quarter as result of the sanctions imposed on exports to Russia. At the same time many companies are lacking materials – a situation that is worsening. According to Statistics Denmark, almost two-thirds of industrial companies are experiencing constraints in their production due to lack of materials. It is expected to affect exports of goods in the coming months.

Source: Statistics Denmark and the Confederation of Danish Industry

Exports of services are back at the same level as prior to the corona crisis, when calculated in current prices. This is mainly due to the increase in freight rates, which have helped boost export revenues from maritime transport. When calculated in constant prices, exports of services have yet to recover completely. The end of Covid-19 restrictions in Denmark and in large parts of the countries abroad provides a fertile ground for a relatively strong growth in service exports. This is especially the case for aviation and tourism, where exports have remained lower than prior to the corona crisis. In recent months, the number of air-crafts in Danish airspace has increased and is currently 15 percent below the level in 2019.

Total exports of goods and services are expected to grow by just over six percent in 2022 and by a further 3.5 percent in 2023.

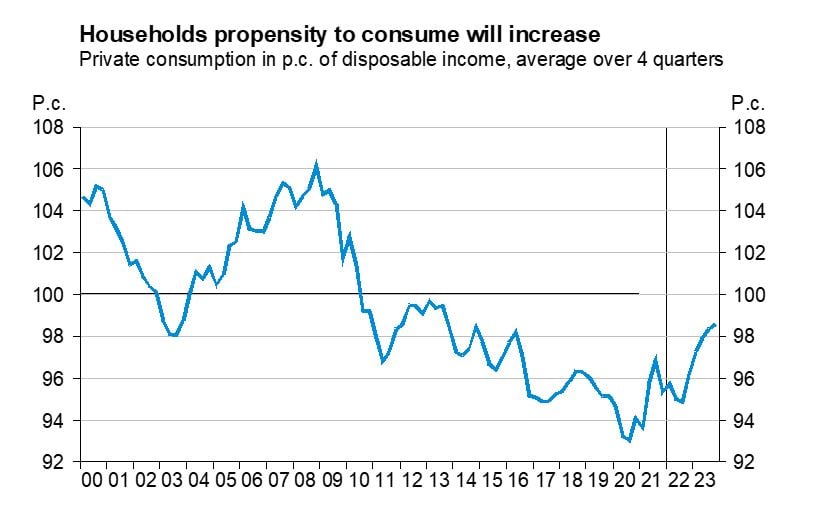

Uncertainty in households imposes a negative influence on private consumption

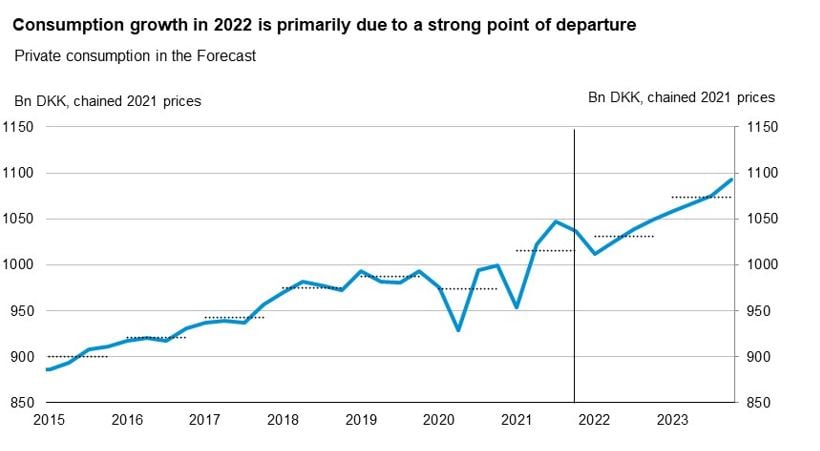

Household consumption grew sharply during 2021, from a poor starting point due to the extensive corona restrictions. However, at the end of the year, private consumption recovered from the corona crisis allowing growth in private consumption at 4.2 percent, this being the highest level of real growth since 2004. Thus, private consumption in 2022 had a very good starting point.

Note: The vertical dashed lines are annual averages. Observations on the right-hand side of the vertical line is the estimate of DI.

Source: Statistics Denmark and the Confederation of Danish Industry

However, several factors stand in the way of growth in private consumption being just as high in 2022. The high level of consumer prices weakens the purchasing power of consumers and erode the real value of the savings accumulated during the corona pandemic. At the same time, consumer confidence, which usually is a good indicator of the development in private consumption, is at its lowest level in more than 30 years. The high level of uncertainty in households therefore indicates a decline in private consumption. However, this time around the decline is estimated to be somewhat smaller than consumer confidence indicates.

This must, among other things, be seen in the light of figures from Danske Bank’s Spending Monitor. They indicate that “Dankort-revenues” in 2022 is nominally stable at around 9 percent above the same period in 2019. However, during the same three-year period, consumer prices have increased by 8.2 percent, which in reality means that this by and large is a stand-still. The high level of consumer prices means that the stable, nominal consumption will lower private consumption in real terms.

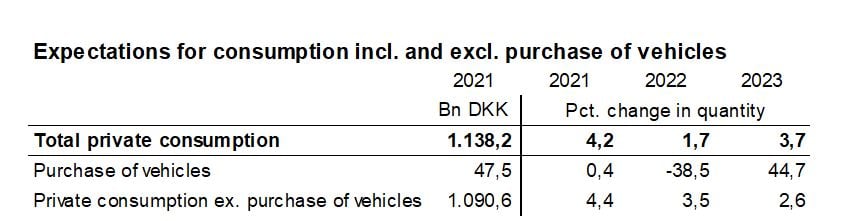

It is not only the demand that is indicating a lower level of private consumption. The continued corona lockdowns in China limits production and thus the possibilities for certain types of consumption. Particularly car manufacturers are very challenged by a shortage of components, which has resulted in long delivery times for cars. The number of newly registered cars in households has therefore decreased by 60 percent from the fourth quarter of 2021 to the first quarter of 2022. In 2021, the purchases of vehicles amounted to 4.3 percent of total consumption, thus the weak level of car sales is expected to have an impact on private consumption in the coming quarters. The lower level of car purchases is expected to be of a temporary nature as it is related to supply problems. Thus, the purchase of cars is expected to increase again as the supply of cars increases, as there is nothing to suggest a significant change in Danish consumers consumption of cars.

Note: Changes in 2022 and 2023 are the estimates of the Confederation of Danish Industry.

Source: Statistics Denmark and the Confederation of Danish Industry.

It is assumed that during the forecast period, the consumption ratio will continue its recovery towards a more normal level roughly corresponding to the level in the period from 2011 to 2015. This recovery must be seen in the light of both nominal price increases and a real increase in private consumption.

Although both supply and demand will put pressure on household consumption in the coming quarters, consumption will be supported by a continued high level of employment and a not insignificant buffer in the increases in wealth experienced by households during the corona pandemic. A number of house-holds will see their purchasing power supported by the agreed payment of the so-called “heat-cheques” in the late summer of 2022 and especially later in the forecast period with the planned repayments of property taxes.

DI estimate that in 2022 private consumption will actually grow by 1.7 percent, while in 2023 growth will be 3.7 percent.

Source: Statistics Denmark and the Confederation of Danish Industry

The high rate of inflation and rising interest rates create extraordinarily great uncertainty about the development in consumption. Both short-term and long-term interest rates have risen sharply during 2022. Rising short-term interest rates increase interest rate payments on all loans with current interest rate adjustments. On the other hand, the increase in long-term interest rates provide opportunities to reap substantial capital gains in connection with loan conversions.

Slowdown in the construction industry, however with continued need for further investments in equipment

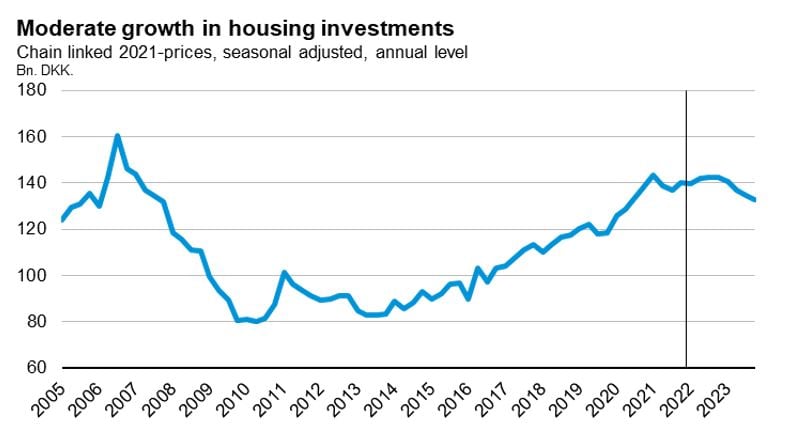

During the corona crisis and lockdowns, the demand for housing has been at an extraordinarily high level. The high demand has affected housing prices and the activity in the renovation market.

A significant factor that will affect the Danish consumer demand are the rising interest rates, which will dampen the consumers’ desire for and opportunity to buy a home, as it will be more expensive to borrow money. It is therefore expected that the demand for housing will now return to a more moderate level.

Russia’s invasion of Ukraine and its consequences also risk slowing down investments in housing and other buildings. This is mainly because companies’ supply chains have been disrupted by the war, leading to a shortage of materials and higher prices.

Despite pressure on capacity, rising inflation and interest rates, the vast majority of construction projects that are either planned or already launched are expected to be completed this year.

Rising prices on materials are, however, expected to affect the initiation of new public housing projects to a great extent, seeing that there is a limit on the maximum price for construction per square meter in order for public construction to receive state aid.

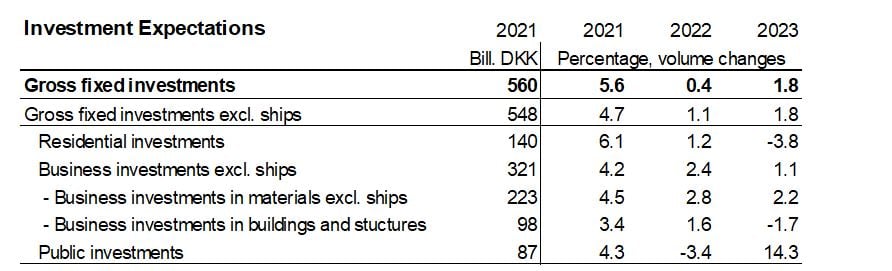

The confederation of Danish Industry expects investments in housing to increase by a modest 1.2 percent in 2022 and to decrease by 3.8 percent in 2023.

Source: Statistics Denmark and the Confederation of Danish Industry

Businesses’ investments in constructions underwent a sharp increase during the corona crisis and is currently at a high level. However, rising prices on energy and on materials in combina-tion with disruptions in the supply chains as well as a shortage of skilled labour have increased the capacity pressure in the

industry. As a consequence, this pressure may result in significant waiting times in relation to the completion of construction projects. Therefore, a slowdown in construction activity in relation to the building of homes, buildings and other facilities is expected in both 2022 and 2023. The Fehmarnbelt Fixed Link, the green conversion of the supply area and the infrastructure plan will, however, pull in the opposite direction and contribute positively to investments in buildings and in constructions in the coming years.

Businesses’ investments in buildings and in constructions are expected to increase by 1.6 percent in 2022 and then to decline by 1.7 percent in 2023.

Source: Statistics Denmark and the Confederation of Danish Industry

Uncertainty about the future activity in the economy, increased production costs and currently also rising interest rates may lead to a lower level of investments.

Despite the fact that the war in Ukraine is expected to have a dampening effect on the economy and on corporate investments, the current “mood” in companies does not yet appear to have suffered any damage. This is, among other things, reflected in the fact that business confidence remains at a high level. At the same time, the high level of activity in the economy puts pressure on companies’ production capacity, which give rise to companies’ need for investments. In addition, the high prices on energy are expected to lead to substantial investments in energy conversion and in energy-saving initiatives, which will also contribute to the companies’ investments in the coming years.

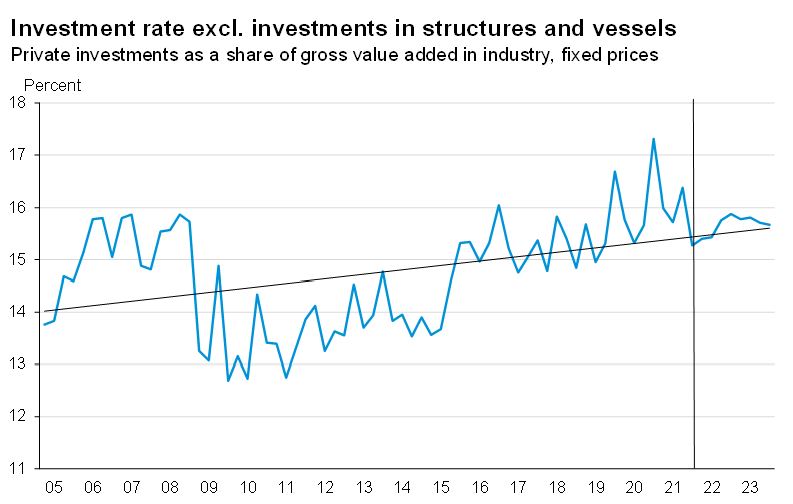

Companies’ investments in equipment (vessels excluded) are estimated to increase by 2.8 percent in 2022 and by 2.2 percent in 2023. The investment ratio is expected to remain at a level similar to the historical average since 2005.

Source: Statistics Denmark and the Confederation of Danish Industry

Although companies’ level of investments currently is generally higher than what we saw prior to the corona pandemic, employment has increased to such an extent that the amount of capital per employee last year dropped. This indicates that companies need to increase their investments in both machinery and equipment, in means of transportation as well as in intel-lectual property rights, such as software and R&D, in order to maintain the same level of investment per employee. This is especially true for small and medium-sized companies, which for years have lagged far behind the large companies in terms of investments.

Businesses’ investments in total (excluding vessels and animals for breeding) are estimated to increase by 2.3 percent in 2022 and by 1.0 percent in 2023.

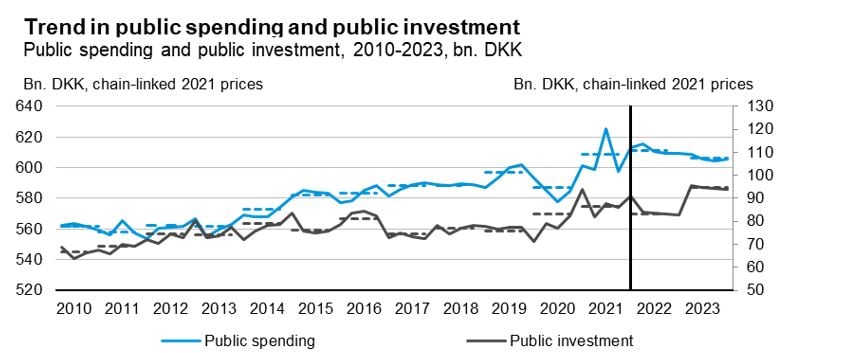

Increase in public spending

According to preliminary figures from national accounts, public consumption in 2021 was almost DKK 610bn, corresponding to a real growth of 3.7 percent in comparison to the previous year. Real growth in public consumption is estimated to be 0.8 percent in 2022, followed by a decline in 2023 of 0.3 percent.

As a consequence of the war in Ukraine, it is expected that public consumption will increase. This is due to expenses for refugees from the war, and due to the fact that money has been set aside for a national security reserve in connection with Danish security policy.

We saw a considerable increase in public investments during the corona crisis in order to help stimulate Danish economy. Real growth in public investment in 2021 was 4.3. percent. As for 2022, a decline in public investments of 3.4 percent, followed by an increase of 14.3 percent in 2023 is expected. The high level of growth in 2023 must be seen in the light of the fact of the delivery of new fighter jets. Both public consumption and public investments are based on the Ministry of Finance’s Economic Report from May 2022.

Note: The horizontal dashed lines indicate annual averages. The level of public investment is shown on the secondary axis.

Source: Statistics Denmark and the Confederation of Danish Industry

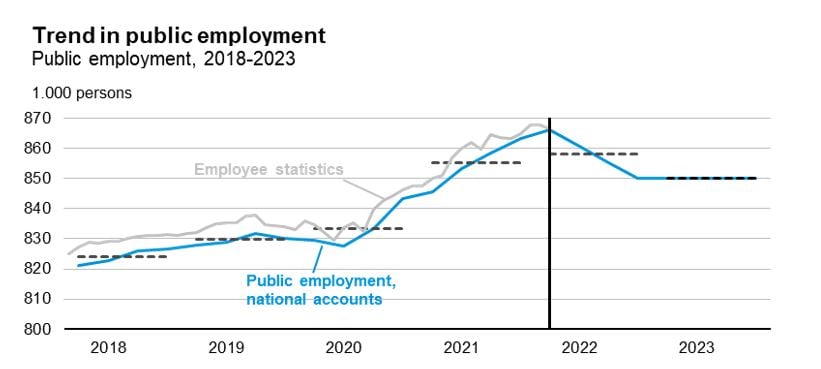

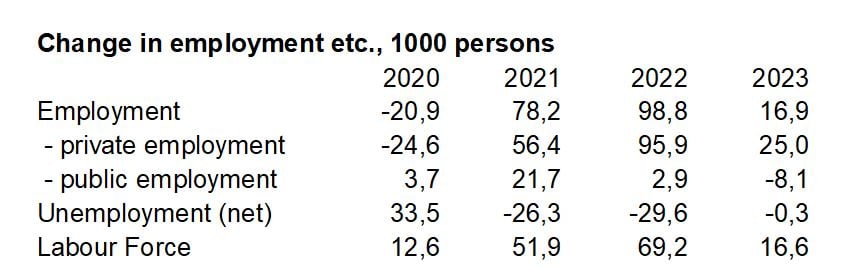

Public employment rose sharply during the corona crisis and is estimated to 863,000 individuals by the end of 2021, corresponding to an increase of 33,000 individuals compared to the fourth quarter of 2019. Some of these jobs were related to testing and vaccination in connection with the corona crisis, but it also covers a general growth in the number of public employees.

Public sector employment increased by almost a further 3,000 individuals from the fourth quarter of 2021 to the first quarter of 2022. In that light, the government’s estimate for public employment in 2022 of 849,000 individuals does not seem realistic. We, therefore, estimate public employment to be 858,000 individuals this year. In 2023, we assume that public employment is in line with the Ministry of Finance’s forecast of 850,000 individuals. This implies a significant boost in public employment from 2019 to 2023, which is not driven by the corona pandemic.

Note: The horizontal dashed lines indicate annual averages.

Source: Statistics Denmark and the Confederation of Danish Industry

The labour market has yet to show signs of a slowdown

Despite increasing uncertainty about the developments in the economy there are still no signs of the labour market deteriorating.

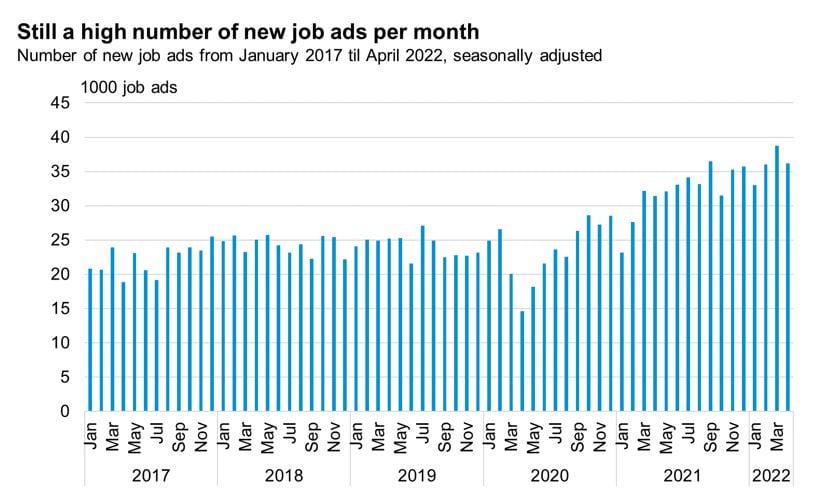

In two years, employment has increased by 159,000 individuals and is at a record high level. At the same time, unemployment in March dropped to 2.5 percent. In the case of unemployment, we need to go back to the middle of 2008 in order to find a lower level. The Ministry of Employment has also published daily figures for registered unemployed until mid-May, and they also point in the direction of a continued declining trend in unemployment. Labour shortages also remain a major issue. In April, more than 40 percent of the companies in both the industry, construction and service sectors stated that they suffer production constraints due to lack of labour.

The number of new job ads has also remained at a very high level throughout both March and April, so it does not in any way indicate that companies have become more reluctant to recruit new employees after the initiation of the war in Ukraine.

Source: Jobindex.dk and the Confederation of Danish Industry

Although everything seems to be looking good in the labour market, the economic outlook has become more uncertain, and it must be expected to have a dampening effect on the labour market. However, the starting point is good, and with the extent of labour shortage we see, it is not given that we are facing any significant increase in unemployment.

Overall, a very large increase in employment from 2021 to 2022 of 99,000 individuals is expected. However, a very large part of this increase has already taken place, as 2021 ended with an employment level 75,000 individuals above the average for 2021. A development that continued in the first quarter of 2022. From the level at the end of the first quarter, only a modest increase is expected for the rest of 2022. When it comes to 2023, the expectation is that on average for the year, employment will be 17,000 individuals higher than in 2022. The development in the economy and thus also in the labour market is currently characterized by extraordinarily great uncertainty.

Source: Statistics Denmark and the Confederation of Danish Industry

Unemployment is expected to drop by almost 30,000 individuals in 2022. In 2021, unemployment ended at a level that was 34,000 individuals lower than in 2021 as a whole. A stagnation of unemployment at the current level is expected for the remainder of 2022 and for 2023.

Source: Statistics Denmark and the Confederation of Danish Industry

The workforce as a total is expected to grow by 69,000 individuals in 2022. This increase follows an almost equally big increase in 2021 of 52,000 individuals. For 2023, a more normal increase in the workforce of almost 17,000 individuals is expected. An increase in the retirement age regarding pension and early age retirement schemes and the influx of employees from abroad contribute positively to the development of the workforce in 2023, while the right to early retirement (for certain groups in the labour market), which was introduced at the beginning of 2022, pulls in the other direction.

Source: Statistics Denmark and the Confederation of Danish Industry

Approach

This economic forecast is based on published Danish and international statistics on national accounts, foreign trade, financial conditions, etc. We have applied the macroeconomic model MONA when carrying out this forecast. MONA has been developed by the Danish Central Bank. However, this forecast and its assessments, are solely the responsibility of the Confederation of Danish industry.

The forecast has been finalized on Friday, May 20, 2022.