Economic Forecast May 2021: From Crisis to Labour Shortage

2021 began with a new and long closure, but all indicators point to the fact that we are in the middle of a quite rapid recovery, as restrictions are lifted. Despite the slow start of the year, there is prospect of a quite reasonable growth in GDP in 2021 of 2.5 percent and employment is estimated to reach a new record high this year.

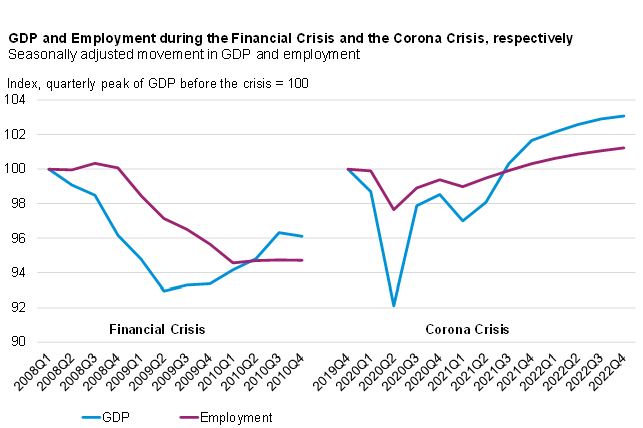

The corona crisis has proved to be a deep, but brief crisis. The downturn in the economy is clearly related to lockdowns and other restrictions imposed to help contain the risk of infection. Thus, the corona crisis is very different from the financial crisis.

Source: Statistics Denmark and Confederation of Danish Industry

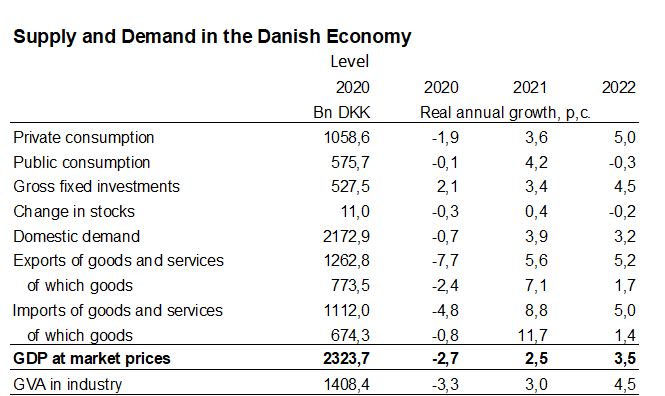

The crisis has not been triggered by structural imbalances in the economy, and therefore demand is picking up rapidly as soon as restrictions are lifted. After a decline in the first quarter, we estimate an overall growth of 2.5 percent in 2021, followed by a further increase of 3.5 percent in 2022.

At the same time, the prospect of a rapid return to normal production levels has meant that companies have not had to lay off employees to the same extent as during previous crises. Although wage compensation and division of labour have not come free-for-all, it has made it possible for companies to keep on employees during periods with a decline in turnover. As a result, employment may already be at a record high level during the second half of 2021. And already now more and more industries are reporting a shortage of qualified employees.

As society reopens, the economy is expected to be refueled. Thus, growth is expected in both investments and exports as well as in private and public consumption in 2021.

Note: Changes in stocks as a percentage of GDP in the previous year

Source: Statistics Denmark and the Confederation of Danish Industry

Even though we are facing a broad-based recovery of the Danish economy, there are still industries that are being held back. This is, particularly the case for areas such as passenger transportation, tourism and for the leisure industry, where customers are still unable to return in a normal scale.

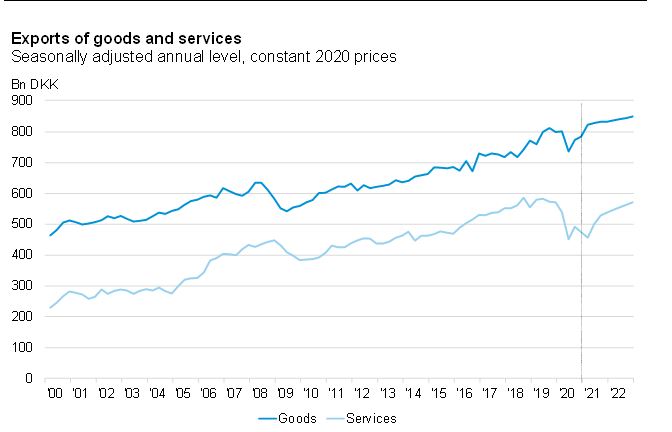

Exports at different pace

Exports of goods have done surprisingly well during the second shutdown. During winter, many restrictions have been introduced in both Denmark and abroad, nevertheless there was an increase in exports of goods in the first quarter. This is not least due to the fact, that sectors such as manufacturing and the construction industry have only been affected by closures to a limited extent. Sectors both of which constitute very significant customers for Danish industrial products. Exports of goods are expected to grow by 7 percent in 2021, while growth is expected to be less strong in 2022. It is expected that the market shares gained during the corona crisis are of a temporary nature sustained by the Danish export mix.

Source: Statistics Denmark and the Confederation of Danish Industry

Service exports were weakened by recent shutdowns. Aviation and revenues from travel are greatly reduced and have a long way back to normal levels. Travel restrictions have cut two-thirds of export revenues from tourism and aviation.

During the last year, export revenues from aviation and travel have been reduced by DKK 56bn compared to the previous year. The tourism industry is in urgent need for us to be able to start traveling again soon, otherwise they will remain unable to reboost their turnover. Increased use of online trade and virtual meetings is making it quite uncertain whether the volume of business will ever return to the same level as prior to the corona crisis.

Travel restrictions are also affecting parts of the exports of goods, as they prevent companies from completing orders, taking in new orders, or carrying out services on products abroad according to service agreements. This is probably particularly the case for small and medium-sized enterprises, seeing as they do not have a large global network and therefore cannot circumvent travel restrictions with the aid of increased efforts by local offices.

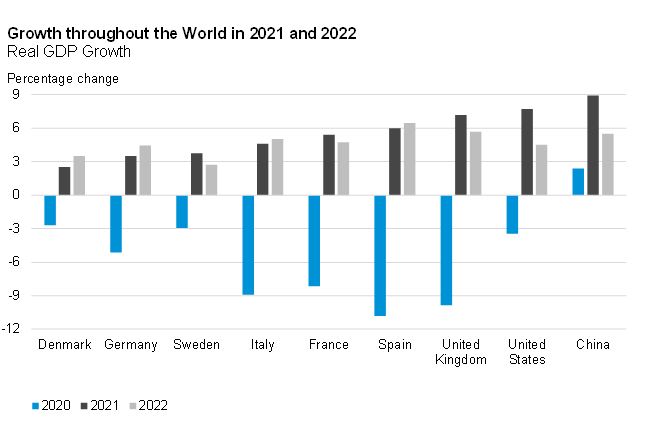

The world economy shrank by almost 3.5 percent in 2020 thus making it the biggest downturn since World War II. However, the world economy is expected to recover in 2021 with growth of over six percent. Growth is expected to be highest in Asia and in the US, but there will be very nice progress in all parts of the world.

Source: Oxford Economics and the Confederation of Danish Industry

As for Europe, coming years’ growth in 2021 and 2022 will be highest in the countries that lost the most in 2020. Danish economy got through 2020 with less economic losses than the other European countries meaning that the way back to normal levels is somewhat shorter thus resulting in a less powerful economic recovery in Denmark.

In coming years, the EU Recovery Fund will accelerate investments in climate and digitalization, areas in which Danish companies hold a solid position. The Recovery Fund is expected to help increase Danish exports by DKK 11bn a year for the next six years. Furthermore, Joe Biden has presented plans for major investments in climate and infrastructure in the US.

Overall exports are expected to increase by just over 5.5 percent in 2021 and by 5 percent in 2022. This means that at the begin-ning of 2022 exports will be back at the same level as prior to the corona crisis (calculated in constant prices).

Solid foundation for a recovery in private consumption

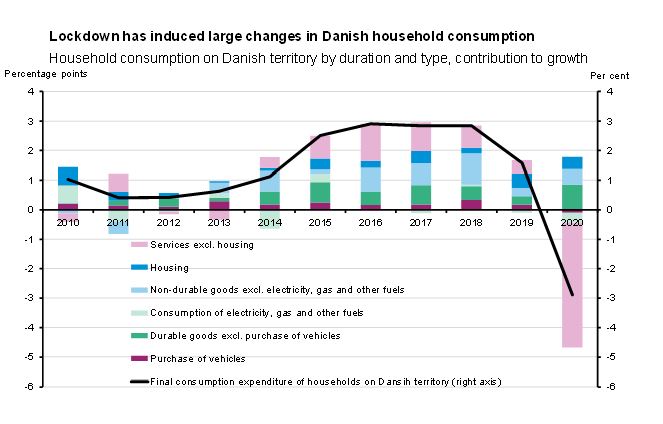

The increase in infection rates during the winter months and the shutdown to help curb further spread of the infection have led to a decline in private consumption in the first quarter of 2021. Figures for credit card revenues stemming from the Spending Monitor from Danske Bank suggest a decline of around 4.5 percent compared to the first quarter of 2020. How-ever, credit card revenues do not cover all household consump-tion. Fixed payments for e.g. housing, insurance and subscrip-tions typically take place via payment services, which is why it must be assumed that the decline in total private consumption has been somewhat smaller than the decline in spending with credit cards.

Not surprisingly, it is in the leisure industry that credit card rev-enues have undergone the sharpest decline. In 2020, the de-crease in consumption of services (housing excluded) contrib-uted to more than the total decline of household consumption in Denmark, while households’ purchases of goods helped boost private consumption. The major changes in Dane’s consump-tion mean that there are big differences in how companies emerge from this health crisis.

Source: Statistics Denmark

The wage compensation scheme has helped sustain household’s disposable income allowing for the decline in consumption to be countered by a higher savings ratio. With the ongoing reopening of society, household’s large savings could be a springboard for a swift recovery of private consumption. The “defrosting” of large parts of the remaining (frozen) holiday pay will also help in supporting this.

Source: Statistics Denmark and the Confederation of Danish Industry

Consumer’s savings are huge and wealth has also risen due to increases in both house prices and prices of equities. The strong wealth position and rising employment will form the basis for growth in private consumption in coming quarters. We therefore expect private consumption to increase by 3.6 percent in 2021 and by 5.0 percent in 2022, thus resulting in the highest growth in private consumption since 1994.

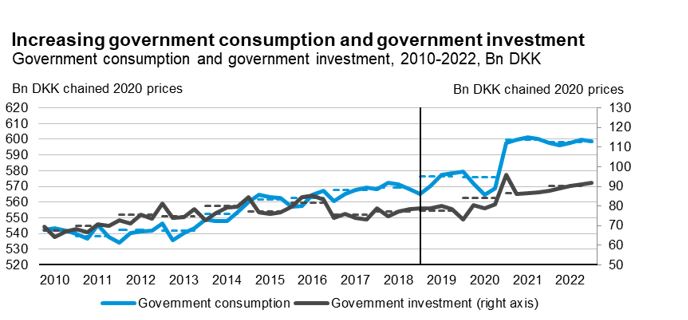

Strong growth in public consumption in 2021

From a political point of view, plans were made for a relatively high level of real growth of 1.3 percent in public consumption in 2020. In addition, the corona crisis has meant that the public sector has made large purchases of protective equipment, vaccines, etc. in 2020, which has added further to public consumption. However, real growth still finished at -0.1 percent according to published national account figures for 2020. This being mainly due to the fact, that the many public employees who were sent home without the possibility to work from home in the spring of 2020 are not included in the calculation of real public consumption.

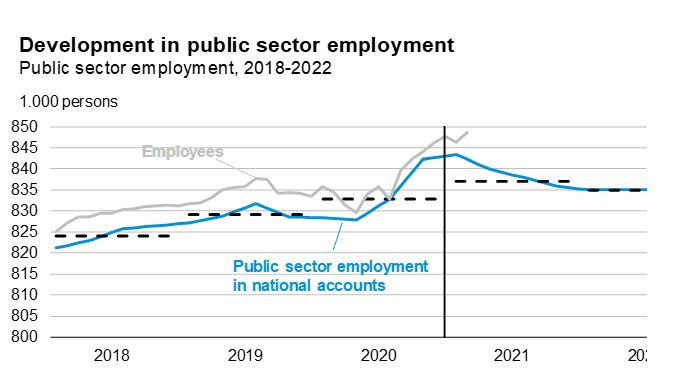

Public employment as calculated in national accounts increased to 832,800 individuals in 2020, which is the highest level since 2011. This is an annual increase of approximately 3,800 individuals, but the growth during the year has been approximately 14,000 individuals (from the fourth quarter of 2019 to the fourth quarter of 2020). Data on public sector employment for the first months of 2021 show a continuation of the increase. The high level of public employment contributes to increasing pressure on the labour market.

Note: The horizontal dashed lines are annual averages

Source: Statistics Denmark and the Confederation of Danish Industry

DI estimates that throughout 2021 public employment will gradually decline to around 836,000 individuals in the fourth quarter as the need for additional healthcare staff in particular decreases. Because employment at the beginning of the year was high, we estimate an annual level of approximately 839,000 individuals in 2020. At the same time, there are also other high temporary costs associated with COVID-19.

Earlier in the spring, the government decided to ease fiscal policy in 2021 by a further 0.1 percent of GDP, corresponding to DKK 2.4bn. The government has used this relaxation of the fiscal policy to increase the so-called “Recovery Fund”, which is why the specific implementation of the extra funds is not yet known. In our forecast, we have assumed that DKK 1.4bn is included in public consumption and DKK 1bn in public subsi-dies. Overall, we estimate a growth in public consumption of 4.2 percent in 2021. In 2022, we estimate a growth of -0.3 percent, which reflects the level of public consumption that the Ministry of Finance expects.

Note: The horizontal lines are annual averages

Source: Statistics Denmark and the Confederation of Danish Industry

Public investments went up by 8.3 percent in 2020 due to a large increase from the third to the fourth quarter, which, among other things, could be a reflection of the fact that municipalities and regions were given free rein to carry out construction projects in 2020. As for 2021 and 2022, our estimate regarding real growth in public investments are of 3.3 percent and 4.2 percent respectively. In 2021 the growth is, among other things driven by the fact that a continued high level of municipal investments is planned with the municipal agreement for 2021. Simultaneously, money has been set aside for public investments in buildings and other facilities, including energy efficiency improvements for public buildings, in the Finance Act for 2021. As for 2022, the forecast is based on the framework for investments included in the projection of the Ministry of Finance. The frame for investments remains high which, among other things, must be seen in the light of the fact that funds have been allocated for the government’s infrastructure plan.

Increase in private investments in the coming years

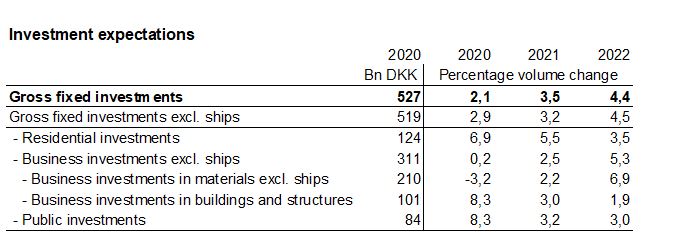

When the corona crisis hit, investments dropped both at home as well as in the countries around us. In particular companies’ investments in equipment, such as machinery and means of transport, suffered quite a significant drop in the first half of 2020. However, there was an increase in investments in buildings and constructions. Since then, investments in equipment have recovered much of what was lost allowing for investments (excluding vessels, etc.) as a whole, to remain at a largely unchanged level in 2020 compared with the previous year.

Although companies’ investments so far have fared relatively well during the crisis, there is still the risk that companies will hold back on their investments. Especially if the health crisis should drag on and we keep having delays in the vaccination program. In particular small and medium-sized enterprises may experience declining investments. A survey among DI members at the beginning of the year showed that SMEs expected to have to step on the brakes when it comes to new in-vestments in 2021.

However, overall business investments are expected to develop positively in 2021. The positive prospects for growth due to the roll-out of vaccines and the consequent reduction in uncertainty as well as increased capacity utilization allow for a nice increase in investments throughout 2021 and in 2022. Overall business investments (excluding vessels and breeding animals) are expected to increase by 2.4 percent in 2021 and then by a further 5.4 percent in 2022.

Source: Statistics Denmark and the Confederation of Danish Industry

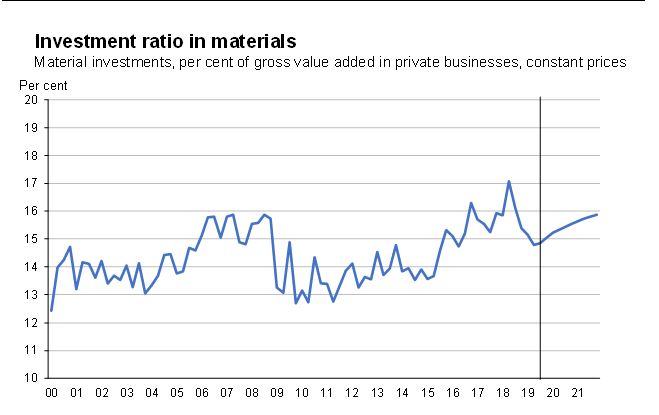

Businesses’ investments in equipment are expected to increase in both 2021 and 2022 in line with growth in the economy. This is particularly the case for investments in machinery and means of transportation, which were hit the hardest during the first part of the corona crisis. On the other hand, companies’ investments in digital transformation and research and development (R&D) have been strengthened during the lockdowns, where digital forms of work and meetings have now become more widespread than before the crisis. At the same time there has been a substantial increase in demand for online sales channels. Companies’ investments in equipment (excluding vessels) are expected to increase by 2.1 percent in 2021 and by 6.6 percent in 2022, which will increase the investment ratio.

Note: Investment ratio for materials excl. ships, airplanes and the energy sector

Source: Statistics Denmark and the Confederation of Danish Industry

The construction industry was not affected by corona restrictions to the same extent as other industries and continued the high level of activity that has characterized the industry in the years leading up to the start of the pandemic. Somewhat surprisingly investments in buildings and construction in-creased by as much as 8.3 percent in 2020. A progress that is expected to continue in 2021 and 2022, however, at a slightly slower pace with an estimated growth of 3.0 percent in 2021 and by 3.1 percent in 2022. In particular investments in the supply sector and the initiation of the The Fehmarnbelt connection are expected to offer a positive contribution to investments in 2021 and beyond.

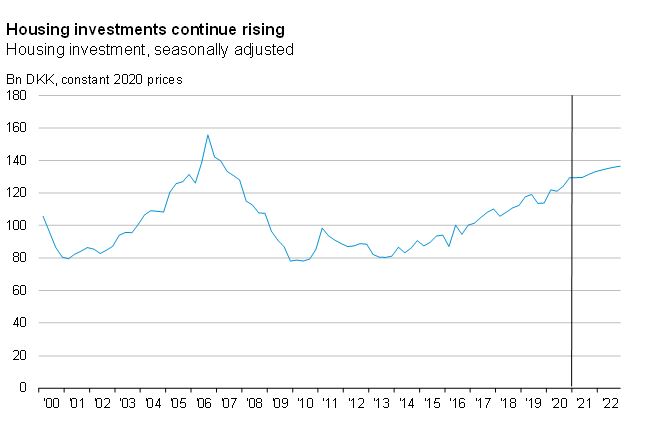

A record number of homes are being built and traded, and the significant activity in the housing market is also expected to continue in 2021. Housing investments have increased significantly in recent years, partly due to high demand, especially in the larger cities, which have contributed to creating high activity in the construction of new housing.

The residential renovation market is expected to characterize housing investments in 2021. The many trades in housing typically lead to high activity in the residential renovation market, as renovations are often carried out in connection with the purchase of housing. The high level of equity, the release of the “frozen” holiday payment, low interest rates and a number of political initiatives, such as the doubling of the “BoligJobordning” in 2021, will help keep activities in the residential renovation market at a high level. Another agreement “Grøn Boligaftale” 2020 is also expected to have significant effect on the renovation market this year and in the years to come. On that basis, total investments in housing are expected to grow by 5.5 percent in 2021 and by 3.5 percent in 2022.

Source: Statistics Denmark and the Confederation of Danish Industry

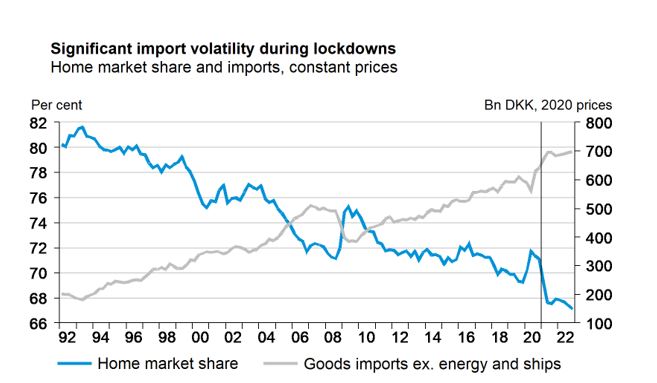

Shutdowns have increased imports

Shutdowns and restrictions have particularly affected tourism, and other areas being significantly dependent on imports. The shutdowns, therefore, led to a significant decline in imports at first. Subsequently, consumption has shifted towards goods such as consumer electronics which are also significantly de-pendent on imports. As a result, we have seen large fluctuations in the import quota.

We expect to see some normalization of the import quota as restaurants and amusement parks, etc. reopen, which will lower the import content. However, in the long run Danes will start traveling abroad again, which will mean increased imports.

Home market share is Danish production for the home market measured as total share of domestic demand.

Source: Statistics Denmark and the Confederation of Danish Industry

Several companies are currently experiencing rising prices as well as a shortage of imported raw materials. The lack of raw materials may delay or even limit companies’ production.

The particularly high level of imports at the beginning of 2021 have led to a certain deterioration in the balance of payments, however the large surplusses have been maintained.

Source: Statistics Denmark and the Confederation of Danish Industry

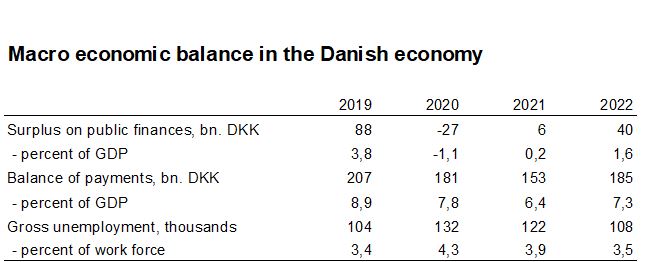

In published national account figures, the public balance shows a deficit of 1.1 percent of GDP in 2020, corresponding to approximately DKK 27bn. This is a surprisingly low deficit after a year of struggling with corona. It is normal for the public balance to deteriorate in times of crisis, seeing that costs for public support schemes increases, while revenues from taxes and duties de-crease when economic activity is low. Compared to the estimate before the crisis, costs for public support schemes in 2020 has increased by DKK 23bn, while around DKK 37bn has been used for (wage) compensation schemes for companies and other COVID-19- related initiatives.

The fact that the deficit did not increase even further in 2020 is mainly due to large revenues from taxing the “defrosted” holiday allowances and as result of the development in financial markets during 2020. According to the Ministry of Finance, the tax revenue from the “defrosted” holiday funds alone, provide a contribution of DKK 20.4bn in 2020 and DKK 13.2bn in 2021.

In 2021 and 2022, the estimates for public surpluses are of approximately 0.2 percent and of 1.6 percent of GDP, corresponding to respectively DKK 6bn and DKK 40bn. The improvement in public finances must partly be seen in the light of the above-mentioned withdrawal/payment of holiday funds, but also to a large extent in the light of the fact that public finances improve in line with the relatively rapid recovery of the economy. The improved economic outlook means less expenses for public support schemes and higher in-come from for example income tax and taxes on consumption such as VAT. Furthermore, the compensation schemes for companies will lapse.

Labour market in rapid recovery

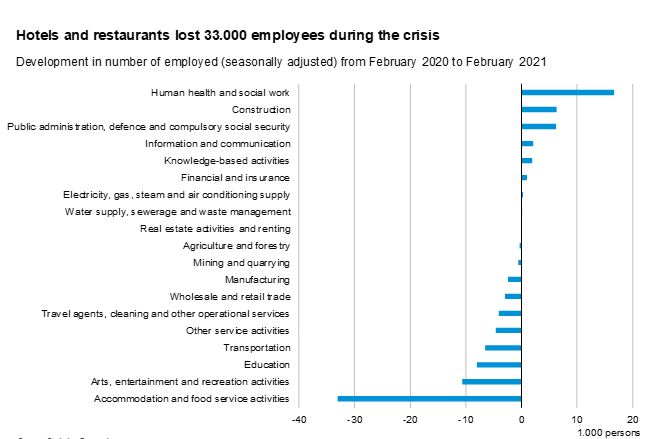

The corona crisis has now for more than a year left its mark on Denmark. However, the effect on the labour market has been far more lenient than one might have feared. In total employment decreased by 38.000 individuals from February 2020 to February 2021.

Developments in employment have varied widely from sector to sector. Hotels and restaurants have taken the hardest blow with its loss of employment of as many as 33,000 employees during the crisis. This corresponds to 27 percent of all employees employed in the sector prior to the crisis. Also sectors such as cul-ture, leisure and transportation are among the hardest hit.

Source: The Confederation of Danish Industry and jobindex.dk

All in all, the development from February 2020 to February 2021 shows a decline in employment of 52,000 individuals in the private sector and an increase of 14,000 individuals in the public sector. Thus, the share of the public sector has grown to 30.7 percent of the employment against 29.8 percent in February 2020.

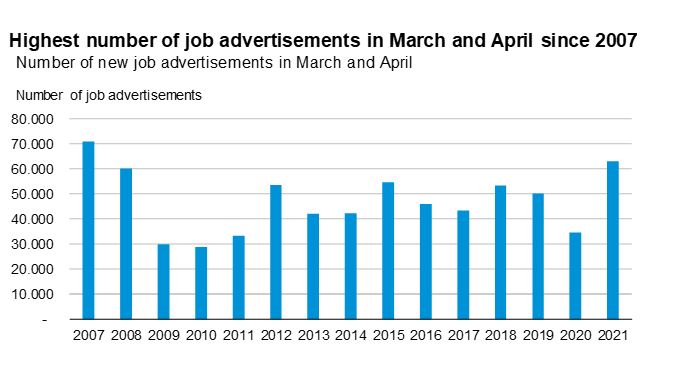

Developments in the spring of 2021 indicate a labour market in good shape. The number of new job adds in March and April has not been seen higher since 2007, and the daily figures for registered unemployment have also shown a clear decline in both March, April and May. The level of unemployment is still higher than before the corona crisis, but the labour market is about to leave the crisis behind. Lack of employees is rapidly on its way to becoming one of the most important agendas for companies again. According to Statistics Denmark’s business survey, the share of companies that experience production restrictions due to shortage of labour is higher than prior to the corona crisis in both manufacturing and the building industry, whereas the service sector remain at the same level as before the corona crisis.

Source: Statistics Denmark

However, there are still industries that have been hit hard by the crisis. Presumably it is the wage compensation scheme, which was reintroduced throughout the whole country on December 9, 2020, which has been able to sustain a significant number of jobs in the experience economy. However, accurate current figures for the scope of the scheme are lacking. Currently the wage compensation scheme stands to being phased out on June 30, 2021.

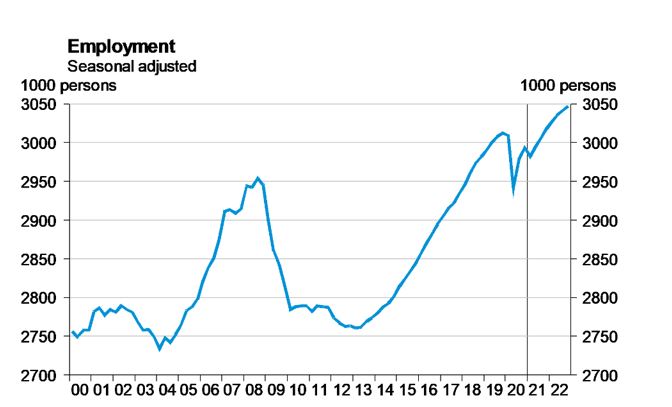

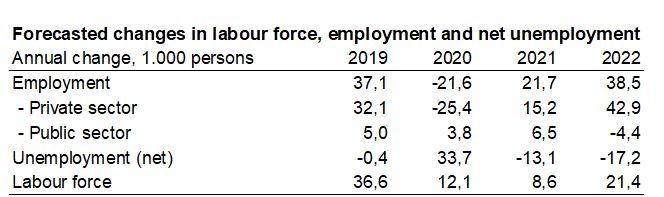

The positive development in employment in connection with the first reopening was declining towards the end of 2020, and in January employment dropped sharply due to new shutdowns. February and March offered a positive development again, but overall a slight decline in employment is expected in the first quarter of 2021. After which there is the prospect of uninterrupted increases during the rest of 2021 in line with the reopening. According to DI’s forecast, employment measured in number of individuals in 2021 will overall arrive at 22,000 individuals higher than in 2020. For 2022 an increase in employment of a further 39,000 individuals, is expected. Thus, during the second half of 2021 employment will again exceed the level prior to the corona crisis and thus be at a record high level. When calculated as full-time employment, we will most likely reach this record even sooner. Already in March, the number full-time employed was just 6,000 individuals below the record level from February 2020. The job loss during the crisis has been smaller when measured in full-time employees, as many of the lost jobs have been concentrated in industries where many people work part-time. This applies not least to jobs in hotels and restaurants.

Source: Statistics Denmark and the Confederation of Danish Industry

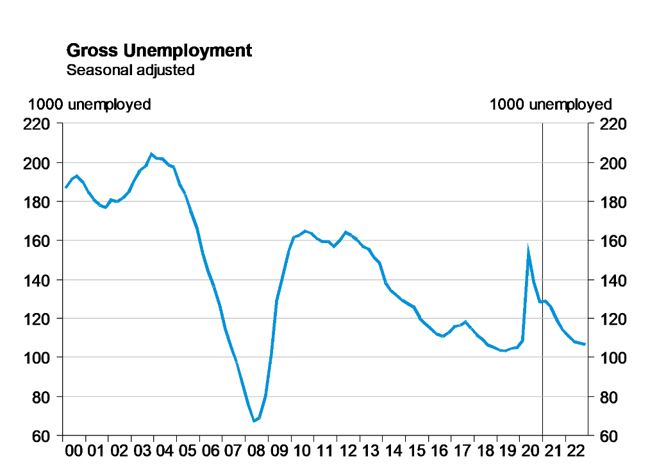

Back in February 2020 – before the corona crisis hit – the unemployment rate was 3.6 percent. Towards May 2020, it rose sharply to 5.5 percent, after which it dropped again for the rest of 2020. In March 2021, which is the most recent month for which figures are available, unemployment is 4.5 percent. Measured in full-time employees, the crisis has led to an increase in unemployment of around 25,000 individuals. In coming months, there is the prospect of decreasing unemployment. DI expects that (gross) unemployment for the whole of 2021, will be 17,000 individuals below the level for 2020. In 2022, un-employment is expected to drop by a further 14,000 individuals.

Source: Statistics Denmark and the Confederation of Danish Industry

An expansion of the workforce of 9,000 individuals is expected in 2021 and a further 21,000 individuals in 2022. An increase in the retirement age, and the influx of foreign employees will have a positive effect on the workforce, whereas the introduction of early retirement in 2022 will have a negative impact. Without early retirement, the labour force would increase significantly more in 2022, and the pressure on the labour market would be lower.

Source: Statistics Denmark and the Confederation of Danish Industry

Approach

This economic forecast is based on published Danish and international statistics on national accounts, foreign trade, financial conditions, etc. We have applied the macroeconomic model MONA when carrying out this forecast. MONA has been developed by the Danish Central Bank. However, this forecast and its assessments, are solely the responsibility of the Confederation of Danish industries.

The forecast has been finalized on Monday, 17 May 2021.